By: Mark Nolan March 27, 2020

The most expensive piece of legislation ever passed on March 27, 2020 when President Trump signed the Coronavirus, Aid, Relief and Economic Security (CARES) (H.R. 748) Act which is his second in less than 6 months after previously passing the SECURE Act, with both greatly affecting retirement plans such as self-directed solo 401k plans, ROBS 401k plans and IRA LLCs.

The Impact of the CARES Act on Retirement Plans Such as Self-Directed Solo 401k Plans, ROBS 401k Plans (A.K.A. Business Financing 401k Plans) and IRA LLCs

Section 2202(a) of the Act: Hardship Distributions

If you are under age 59 1/2 , the 10% early distribution penalty which applies to distributions made prior to the participant reaching age 59 1/2 is waived on distributions up to $100,000. This amount is aggregated for the year and distributions must be made between January 1 and December 30, 2020. If you have multiple retirement plans for businesses that you control, this $100,000 distribution limit applies in aggregate to all plans sponsored by each business.

In order to qualify, it must fall under COVID-19 Related Distribution (CRD)

The Act (see Section 2202(a)(4)(A)(ii) of the CARES Act ) defines a CRD as:

- is diagnosed with COVID-19, with a CDC-approved test;

- whose spouse or dependent is diagnosed with COVID-19, with a CDC-approved test;

- who experiences adverse financial consequences as a result of being quarantined, furloughed, laid off, having work hours reduced, being unable to work due to lack of child care due to COVID-19, closing or reducing hours of a business owned or operated by the individual due to COVID-19; or

- other factors as determined by the Treasury Secretary.

- Individuals are permitted to pay tax on the income from the hardship distributions over a three-year period.

- Individuals may choose to repay hardship distribution amounts back to the plan over the next three years.

- The repayments do not count toward the annual retirement account contribution limits.

Note: COVID-19 distributions do not fall under the hardship distribution category. It falls under its own new category; therefore, none of the stringent plan hardship distribution rules apply.

Tax Reporting

While distributions from 401k plans including self-directed solo 401k and ROBS 401k plans are generally subject to the 20% early income tax withholding requirement, with the proceeds paid to the Department of the Treasury by the 15th of the month following the month in which the distribution occurred, the upfront withholding of this 20% federal tax does not apply to Coronavirus Related Distributions (CRD); however, part of the federal tax will be due when the personal Form 1040 tax return is filed in 2021. VISIT HERE to learn more about paying the taxes due on the distribution over 3 (three) years.

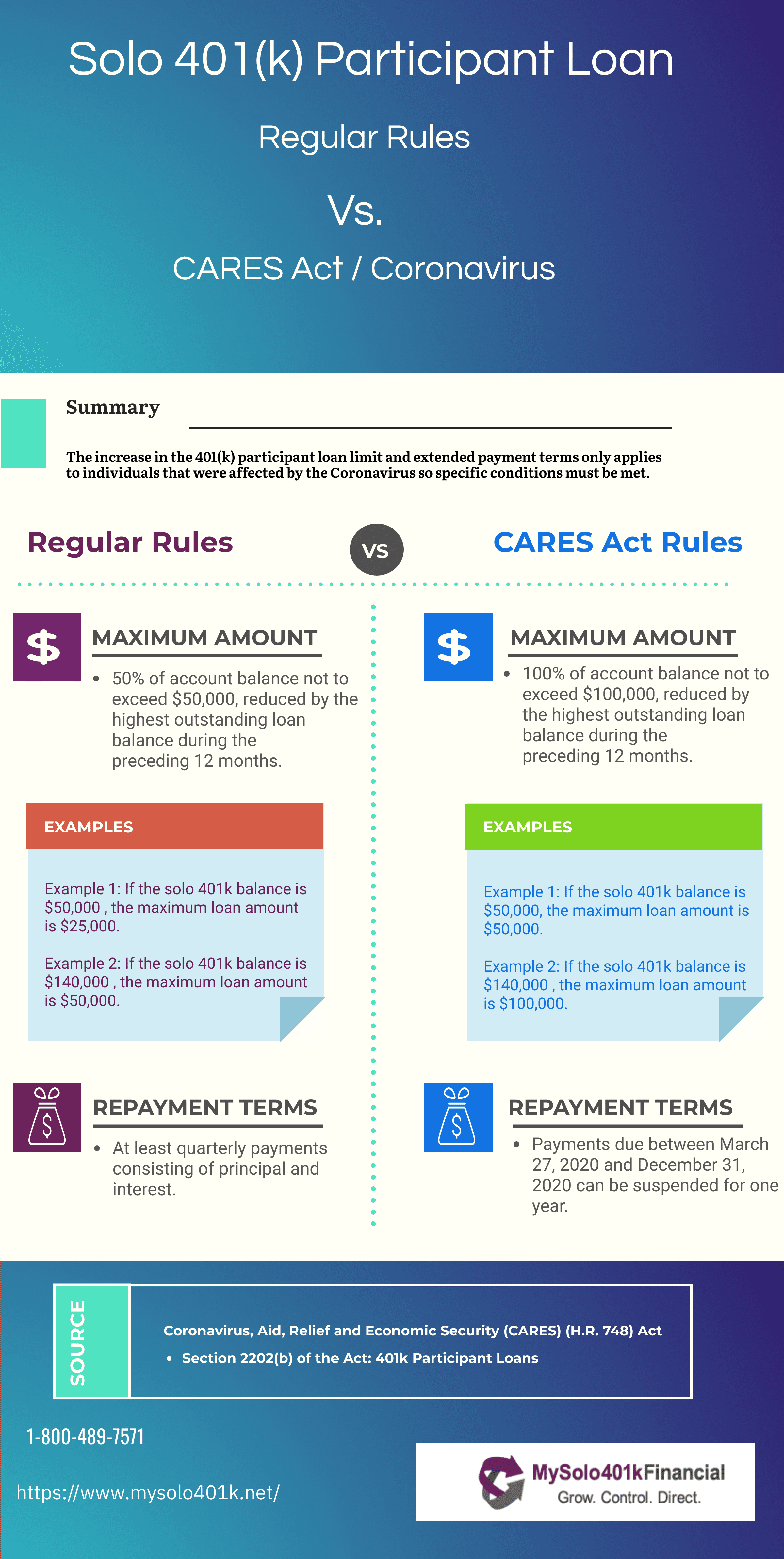

Section 2202(b) of the Act: 401k Participant Loans

An important provision in the CARES Act is the delay of certain solo 401k participant loan repayments.

- For solo 401k and ROBS 401k participants, the loan limit has been increased from $50,000 to $100,000 (reduced by any outstanding loans). IMPORTANT NOTE: This increase in the 401k participant loan limit only applies to individuals that were affected by the Coronavirus so must meed the conditions described above.

- In order to qualify for this participant loan increase, the loans must be made in the 180-day period from the date of the Act’s enactment, and the participant must meet the Coronavirus Related Distributions (CRD) rules mentioned above.

- The participant can borrow based on the total balance of her ROBS 401k or solo 401k plan, so the 50% of account balance rule does not apply.

- The due date for participant loans due between the date of the Act and December 31, 2020 are extended one year.

- Solo 401k and ROBS 401k Participants with outstanding 401k loans due between the date of the Act and December 31, 2020 are extended one year, so can delay their loan payments for one year. VISIT HERE to learn more.

Lastly, solo 401k participants are not required to suspend payments and could continue to make repayments on the solo 401k participant loan.

Section 2203 of the Act: Relief From Required Minimum Distributions (RMD)

- RMDs are waived for calendar year 2020 for 401k plans including solo 401k plans, 403b and 457b plans, as well as SEP and SIMPLE IRAs, Traditional IRAs, Roth IRAs and inherited IRAs. Note that for those who reached age 70 1/2 in 2019 and delayed taking their first RMD until April 1, 2020, will also not have to take it in 2020–it is waived. Lastly, the bill also waives all required minimum distributions for 2020 regardless of whether the participant has been impacted by the Coranavirus.

- Participants who have already taken their 2020 RMD can roll it back to the solo 401k plan or to an IRA.

No Impact on Form 5500 or Form 5500-EZ

As it currently stands, the CARES Act has not impact on the deadline to file Form 5500 including Form 5500-EZ, so the deadline is still July 31, 2020 for calendar year solo 401k and business financing 401k plans (ROBS 401k).

VISIT HERE to read FAQS surrounding the CARES Act.

CLICK HERE for information regarding Notiec 2020-23 which also separately allows for the delay or making solo 401k participant loan payments due during the period of April 1, 2020 to July 14, 2020 and does not require a COVID-19 exception.

IRS released new guidance on June 19, 2020: June 19, 2020 IRS Notice 2020-50

IRS Notice 2020-51 Extends RMD Rollover Period to August 31, 2020

More Information

Spreading the Income Tax Over 3 Years

Deep Dive-Cares Act Distributions & Payback Over 3 Years

June 19, 2020 IRS Notice 2020-50

IRS Notice 2020-51 Extends RMD Rollover Period to August 31, 2020