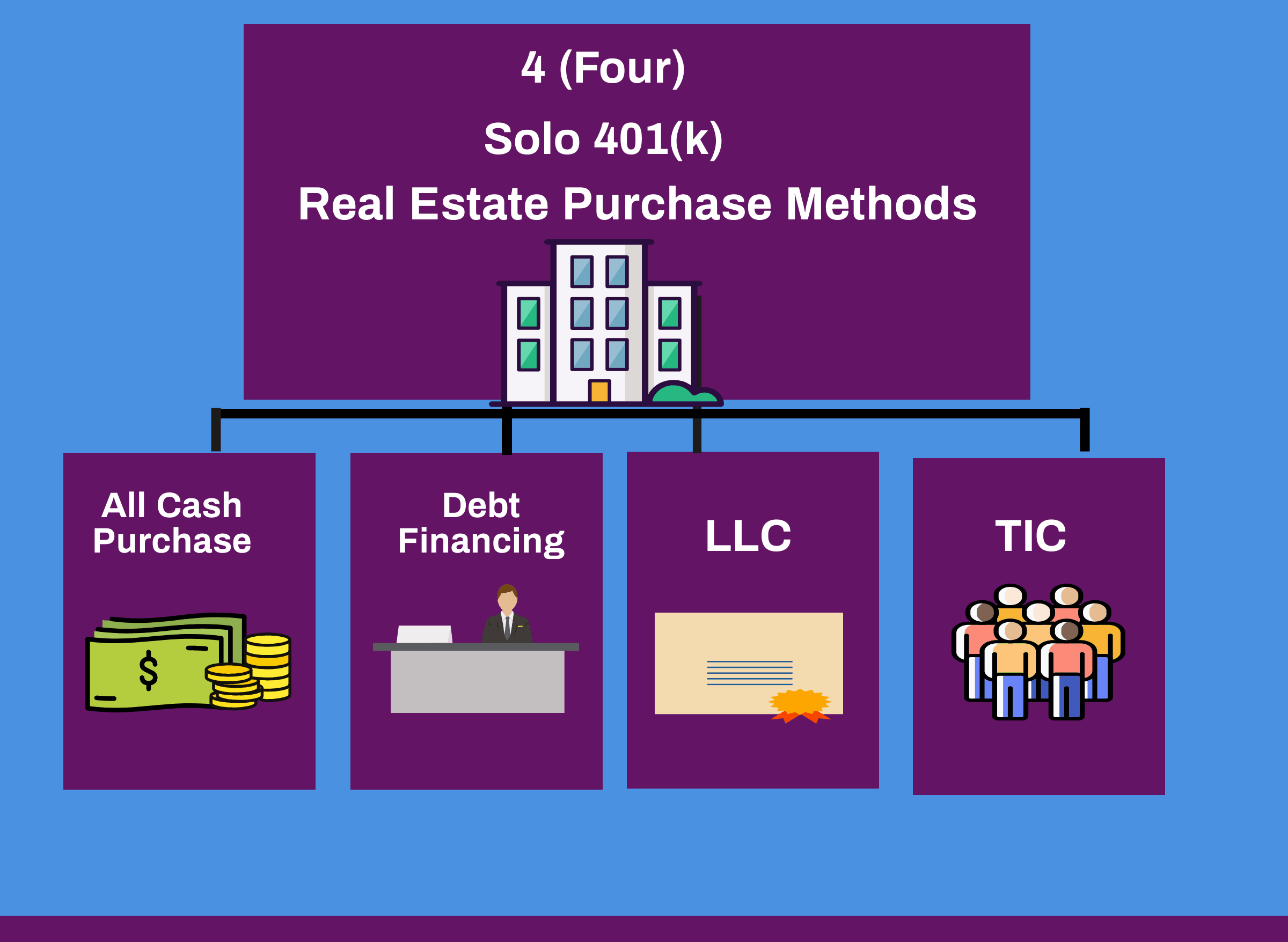

Once the self-directed solo 401k for investing in real estate has been established, the next step is to decide which real estate investment method to use.

If you choose to use debt financing / non-recourse loan, then here are some important compliance items to understand.

- Non-recourse loan means the solo 401k can borrow (take a loan) from a third-party lender (generally a bank or hard money lender) for investing in real estate.

- By using leverage or debt financing, the solo 401k can effectively increase the funds available for investing in real estate.

- Non-recourse means that in the even of loan default the lender will not have recourse against the solo 401k participant / trustee or any other asset of the solo 401k plan. In the event of default / foreclosure, the lender can only recover the real property.

- Non-recourse loans can be obtained through certain banks (e.g., North American Savings Bank) as well as hard-money lenders (e.g., friend, investor, or company specializing in non-recourse loans).

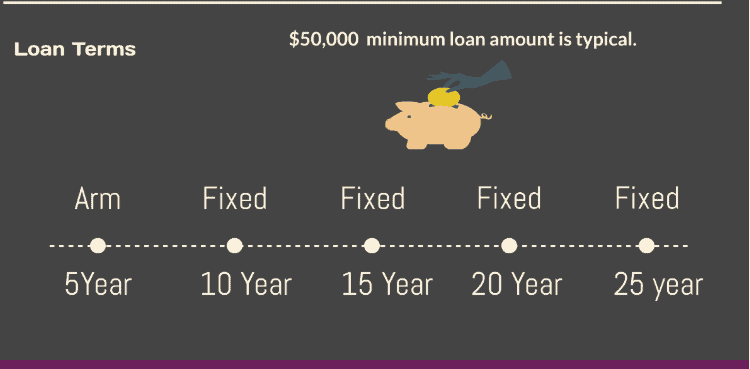

- While non-recourse loans can be structured for any term period, banks that specialize in is this type of loan generally provide fixed interest loans.

- Non-recourse loan frees up cash in your solo 401k for use in other investments including additional real estate purchases because some not all of of the solo 401k funds are used in conjunction with the borrowed funds to invest in the property.

- A non-recourse loan to a solo 401k paln is quite different from a conventional loan in that the bank only review the solo 401k balance and existing holdings, and will not use the following to qualify the loan.

- Will not check to see if you are employed

- Will not check your income

- Will not look at your W-2’s

- Will not look at your tax returns

- The non-recourse loan is to the solo 401k; therefore, the loan does not affect your credit nor does it appear on your credit report. When providing the bank with the necessary solo 401k documents for processing the non-recourse loan, make sure to provide the solo 401k plan’s employer identification number (EIN) and that they use the Plan’s EIN not your social-security number for reporting on their end.

Non-Recourse Loan from Father’s LLC QUESTION:

I see that you mention friend, investor, or company specializing in non-recourse loans. I am considering taking a non-recourse loan from an LLC that is in the name of my father.

While the solo 401k may obtain a non-recourse loan from a bank, hard money lender, or an individual, for example, it would be prohibited for the solo 401k to obtain a non-recourse loan from the solo 401k owner's parents or from an LLC where the parent's are members of the LLC. The prohibited transaction and disqualified party rules apply both directly and indirectly.