Last Updated 4/17/2026

In-kind transfer

An in-kind transfer entails moving the assets (non cash assets such as real estate, private investments, promissory notes, mutual funds, stocks, etc.) from a former employer or current 401k to another 401k such as a Solo 401k Plan. An in-kind transfer is preferred if you do not want to liquidate your investments but still want to transfer assets to a Solo 401k. An in-kind transfer is tax free and can be processed to a Solo 401k Plan before or after the 12/31 Solo 401k establishment deadline.

Cash transfer

Cash transfer is just what it sounds like: you move cash from your former employer 401k to a Solo 401k instead of assets (e.g., mutual funds or stocks). If your 401k is currently invested in mutual funds or stocks, you first have to contact your current 401k provider and request that they sell your mutual fund or stock positions before proceeding with the cash transfer. A cash transfer is not taxable and partial or full amounts may be processed. Lastly, a cash transfer can be processed to a Solo 401k before or after the 12/31 Solo 401k establishment deadline.

In-kind direct rollover

An in-kind direct rollover differs from an in-kind transfer in that assets from an IRA not a 401k are transferred to a Solo 401k. Just like an in-kind transfer, non cash assets (e.g., mutual funds, stocks, real estate, notes, private investments, etc.) are moved to the solo 401k. to a Solo 401k instead of liquidating the investments and then directly-rolling over cash. The movement of funds from an IRA to a Solo 401k is tax reportable but not subject to tax withholding because assets are transferred in-kind to a Solo 401k. Lastly, an in-kind direct rollover can be processed to a Solo 401k before or after the 12/31 Solo 401k establishment deadline.

60-day cash rollover

This method of moving funds from an IRA to a Solo 401k may be the fastest of all available methods; however, it puts more pressure on you because the funds or assets are distributed in your name and mailed to you. You then have 60 days from the date you receive the assets/check to deposit them to your Solo 401k in order to avoid payment of taxes and the 10% early distribution penalty if you are under age 59 1/2. This method also subjects your IRA to tax reporting but not taxes provided the funds/assets are timely rolled over to your new Solo 401k . Lastly, a 60-day cash rollover can be processed to Solo 401k before or after the 12/31 Solo 401k establishment deadline.

NOTE: The above funding methods do not affect the solo 401k annual contribution limits. In other words, you can transfer or rollover as little or as much as you want without affecting your annual solo 401k contribution limit.

Solo 401k Funding Methods Continued

Annual cash contribution

Provided you have income from self-employment and establish the Solo 401k by 12/31 (by executing the plan documents), you can wait to fund the Solo 401k by making an annual cash contribution by your business tax return due date plus extensions. For tax year 2025 the maximum annual contribution limit is $70,000 plus an additional catch up amount of $7,500 if you are age 50 or older. Starting in 2025, those ages 60 to 63 have a higher catch-up contribution limit of $11,250 instead of $7,500 thus resulting in being able to contribute $81,250.

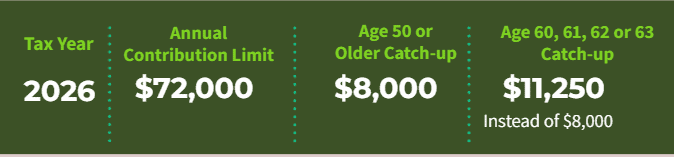

For 2026, the contribution limit increases to $72,000 or $80,000 if age 50 or over (The $8,000 catch-up contribution). The super catch-up amount of $11,250 for those ages 60 to 63 remains the same for 2026.

The contribution limits apply separately to each Solo 401k participant.

Additional Information

Consolidating Retirement Plans:

https://www.mysolo401k.net/consolidating-retirement-plans-using-solo-401k-plan/