The Coronavirus Aid, Relief and Economic Security (CARES) Act impacts solo 401k plans in a variety of ways. Below are some FAQs to help self-directed solo 401k participants navigate the new Act.

Solo 401k Withdrawals

Can solo 401k participants withdrawal their funds due to the COVID-19 pandemic?

Yes, provided it falls under a CRD exception (see Section 2202(a)(4)(A)(ii) of the CARES Act), the withdrawal will be penalty free (i.e., it is not subject to the 10% early distribution penalty). The distribution limit is $100,000 and must be made between January 1, 2020 and December 31, 2020.

How am I eligible for the withdrawal?

In order to qualify, it must fall under COVID-19 Related Distribution (CRD). To qualify for the distribution, the participant, or his or her spouse or dependent, must have been diagnosed with COVID-19 (a CDC-approve trust applies), or the individual suffered adverse financial consequences due to COVID-19 (e.g., closing or reducing hours of business, laid off, reduced work hours, furloughed, unable to work due to lack of child care, etc.).

What if I already paid the taxes due on the distribution?

If you have already paid taxes on a solo 401k distribution that you later decide to repay, you will need to file an amended personal Form 1040 tax return to recover the taxes.

Is there a limit on the distribution amount?

Yes. The limit is up to $100,000 per solo 401k participant. For example, if both spouses hold funds in the solo 401k plan, each can distribute up to $100,000 from their respective participant account under the plan. Also, if you maintain multiple solo 401k plans, the $100,000 is aggregated so it does not apply separately to each plan.

What if I already took the COVID-19 distribution from my IRA?

COVID-19 distributions are aggregated between IRAs and solo 401k plans. Therefore, if you already took the full allowed coronavirus limit of $100,000 from your IRA, then you won’t be able to take a coronavirus related distribution from the solo 401k plan. There are not restrictions on how the distributed funds are used.

Can I repay the amount distributed?

Yes. The distribution can be repaid to the solo 401k plan or to another 401k plan. The solo 401k distribution can also be repaid to an IRA instead. This has to happen within a three-year period following the distribution and it will be treated as non-taxable rollover so that taxes can still be deferred.

Can I distribute Roth solo 401k funds under COVID-19?

Yes. If The Roth solo 401k distribution is non qualified (Click here to learn about the qualified vs non-qualified Roth solo 401k distribution rules.) it will include pro rata share of basis and gains…if qualify under cares act this satisfied as triggering event and will allow the taxable amount not to be subject to penalty and to spread taxes on taxable portion over three years.

Regarding CARES Act 401k/403b withdrawals. Is there any strategy in which one can incorporate Roth conversion into payback of the Solo 401k withdrawal?

Not directly. In paying back the funds the funds must be paid back “like to like” – for example a CARES Act distribution from a pre-tax account must be paid back to a pre-tax account. You could then subsequently process an in-plan roth conversion but the entire amount converted would be taxable in the year of the conversion.

If I have a solo 401k with $200k in it, and a regular 401k (day job) with $200k in it... Can I take a $100k 401k loan from EACH plan ($200k total loans) AND can I withdraw an additional $100k aggregate from either/both plans ($100k max)...So in the end I have $300k in funds ($200k loaned and $100k withdrawn)?

While the coronavirus related distribution (CRD) maximum amount of $100,000 is aggregated between all of your qualified plans (e.g., full-time employer 401k and self-employed solo 401k plan) and IRAs, meaning you cannot distribute $100,000 from each, participant loans from 401k plans are not subject to this same aggregation rule. Therefore, yes the 401k rules allow for taking the maximum of $100,000 from each 401k plan–that is the full-time employer plan and the self-employed solo 401k for a total of $200,000 provided the loans are taken under a COVID-19 exception. Lastly, yes you can process the CRD related aggregate distribution amount of $100,000 in addition to processing the $100,000 401k participant loan amount from each 401k plan.

It’s my understanding that the taxes on COVID withdrawal can be spread out over 3 years. Is that automatically spread out or can I pay it all in year 3? (Asking in case I pay it back before the 3 years to avoid the taxes)?

The federal taxes due on the distribution have to be paid back at minimum equally over 3 years or can be paid sooner. This three year period begins in 2020, the year the distribution was taken. The amount of taxes due on the distribution is based on your total earned income for the year, and distributions from solo 401k plans are taxed at earned income rates.

Example: Jane took a CRD related $90,000 solo 401k distribution on April 15, 2020. Jane can include the full $90,000 distribution as earned income for 2020, or she can can spread it over a three-year period ($30,000 in income for 2020, $30,000 in income for 2021, and $30,000 in income for 2022).

If I took a COVID-19 related distribution in addition to also taking another distribution since I am over age 59 1/2, can I later redeposit my 2nd distribution to an IRA?

Good question and the answer is yes for or two reasons.

First, distributions from solo 401k plans are not subject to the one rollover per year limit like it applies to distributions from IRAs. Therefore, as long as the non-coronavirus related distribution is deposited to an IRA or back to the solo 401k plan within 60 days from the date of the distribution, it will satisfy he 60 day rollover rule.

The second reason is that COVID-19 related distributions are exempt from the one rollover per year rule. See IRS Notice 2020-50 for more information.

I received a Form 1099-R for my 2020 CRD that I took out in 2020 but it has a code 1 in box 7 instead of a code 2, is this correct?

In short, yes it is correct. Code 2-“early distribution exception” does not apply as solo 401k distributions on account of COVID-19 do not fall under the typical hardship umbrella (e.g., disability, death, etc.) nor an IRS levy. If it did, you would be required to pay a 10% early distribution penalty. What is more, hardship distributions cannot be rolled back to a solo 401k or an IRA whereas COVIDE-19 related distributions may be rolled back to the solo 401k or to an IRA.

Therefore, you would not want to use code 2 since the COVID-19 related distributions can be rolled back to a solo 401k or an IRA over three years.

Coronavirus distributions are reported as normal distributions on Form 1099-R. Instead, you as the solo 401k owner/participant will need to report it as rollover on your Form 1040 tax return. The total distribution from the solo 401k must be indicated on line 5a of Form 1040 when filing the federal income tax return. Then enter the taxable amount for the particular year in 5b with the text “CRD” next to the amount entered in 5b.

You will also need to file Form 8915-E to report the COVID distribution and to get relief from the 10% early distribution penalty. Form 8915-E also has a box where you can opt out of the 3 (three) year option to spread the income if you wish to include all the income in 2020.

Quick question - if splitting the taxable income across 3 years, do I have to do so evenly? As in, do I have to claim $33,333.33 in 2020, 2021, and 2022? Or could I claim 34/33/33 or 50/50/0, or some other combination, so long as it totals the $100k?

The federal taxes due on the distribution have to be paid back at minimum equally over 3 years or can be paid sooner. The three year period begins in 2020, the year the distribution was taken. See question 7 on this IRS page.

Solo 401k Participant Loans

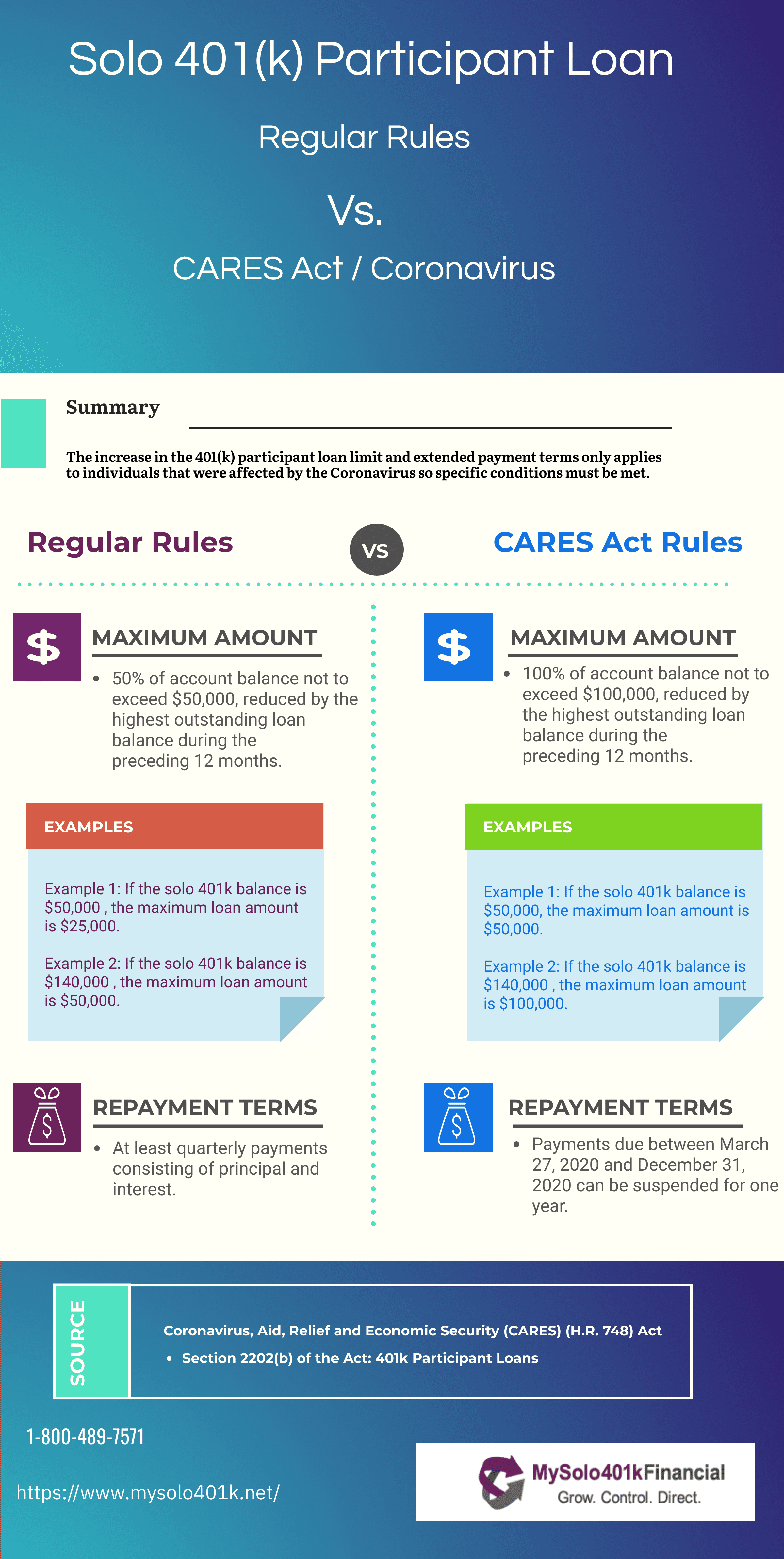

Can I delay making payments on my existing / outstanding solo 401k participant loan?

Yes, but only on payments due from March 27,2020 through December 31, 2020. Solo 401k loan Payments due within this period can be delayed for one year. However, interest will continue to accrue.

How are new solo 401k participant loans affected?

The Act also allows those affected by COVID-19 to take lesser of $100,000 (reduced by outstanding loans) or 100% of the solo 401k account balance. This only applies to solo 401k participant loans made on or before Sept. 23, 2020 (180 days following enactment of CARES Act). You also have to meet the same COVID-19 conditions listed above under the distribution FAQs.

I currently have an outstanding solo 401k participant loan and my self-employed business has been severely impacted by the Coronavirus. Can I delay making 401k loan repayments?

The CARES Act which was enacted to provide relief to individuals impacted by COVID-19 allows for increased 401k loans and more flexibility for repayment of these loans.

Specifically, you must be an individual who meets one of the following conditions to demonstrate that you have been impacted by the crisis (and it will be your responsibility to retain documents in your files that demonstrates that you are a qualified individual):

Individual who is diagnosed with COVID-19, with a CDC-approved test;

Individual whose spouse or dependent is diagnosed with COVID-19, with a CDC-approved test; OR

Individual who experiences adverse financial consequences as a result of being quarantined, furloughed, laid off, having work hours reduced, being unable to work due to lack of child care due to COVID-19, closing or reducing hours of a business owned or operated by the individual due to COVID-19; or other factors as determined by the Treasury Secretary.

If you meet the above conditions:

You may delay making any 401k loan payments due between 3/27/2020 and 12/31/2020.

You must commence making loan payments in January 2021 (or the first quarter of 2021 if your loan payments are due on a quarterly basis).

If you elect to delay making such loan payments, the term of your loan will be appropriately extended. For example, if there are 10 monthly loan payments remaining on your 401k participant loan and the next payment is due April 15, 2020, you can elect to delay making such payments until January 15, 2021 and at that time would need to make 10 more monthly payments through October 15, 2021.

Once the solo 401k has been funded, the solo 401k participant loan can be processed immediately so no waiting period applies.

My self-employed business has been severely impacted by the Coronavirus. Can I take a 401k loan to help cover expenses?

The CARES Act which was enacted to provide relief to individuals impacted by COVID-19 allows for increased 401k loans and more flexibility for repayment of these loans.

Specifically, you must be an individual who meets one of the following conditions to demonstrate that you have been impacted by the crisis (and it will be your responsibility to retain documents in your files that demonstrates that you are a qualified individual):

Individual who is diagnosed with COVID-19, with a CDC-approved test;

Individual whose spouse or dependent is diagnosed with COVID-19, with a CDC-approved test; OR

Individual who experiences adverse financial consequences as a result of being quarantined, furloughed, laid off, having work hours reduced, being unable to work due to lack of child care due to COVID-19, closing or reducing hours of a business owned or operated by the individual due to COVID-19; or other factors as determined by the Treasury Secretary.

On or before September 22, 2020, such individuals take a 401k participant loan subject to the following terms:

Maximum Amount of the Loan: 100% of their 401k balance not to exceed $100,000. Please note that per the multiple loan rules, the amount of the loan must be reduced by the highest outstanding balance of any other 401k participant loan over the prior 12 months (regardless of whether such other loan is currently outstanding).

Monthly or Quarterly Payments: The loan must be paid back in equal monthly or quarterly payments of principal and interest.

Interest Rate: The interest rate is equal to prime plus 1% (or CD rate plus 2%) and is a fixed rate that is set at the time that the loan is taken.

Term of the Loan: Five-year term unless the proceeds of the loan are used to purchase a primary residence in which case the term of the loan may be up to 30 years.

First Payment:

For monthly payments, the first payment that would otherwise be due is delayed until January 2021 (e.g. if the first monthly payment would have been due on May 15, 2020, it will be due on January 15, 2021).

For quarterly payments, the first payment that would otherwise be due is delayed until the first quarter of 2021 (e.g. if the first quarterly payment would have been due on May 15, 2020, it will be due on February 15, 2021).

Can I take another solo 401k participant loan if I already have one outstanding?

While those impacted by COVID-19 virus can take a loan equal to 100% of the balance up to $100k, the multiple loan rules apply if you already have an outstanding from your solo 401k plan. Per the multiple 401k loan rules, the amount of the loan must be reduced by the highest outstanding balance of any other solo 401k participant loan over the prior 12 months (regardless of whether such other loan is currently outstanding).

If I default on my current solo 401k loan in 2020, can I treat it as a taxable distribution under COVID-19?

On June 19, 2020 the IRS released updated guidance in IRS Notice 2020-50 regarding taking distributions and processing 401k participant loans under a COVID-19 triggering event. Prior to this notice, many in the industry understood that if the 401k account holders defaulted on their solo 401k participant loans in 2020 it could be treated as a coronavirus related distribution (CRD); however, in IRA Notice 2020-50 the IRS clarified that 401k participant loans that go into default do not qualify to later be treated as a coronavirus related distribution (CRD). This is an important rule, because CRDs do qualify for the repayment of the distribution over 3 (three) years.

Determine if I Qualify

Does the solo 401k plan provider need to verify if the solo 401k participant qualifies for a COVID-19 withdrawal or participant loan?

No, the onus will fall on the solo 401k trustee to certify eligibility based on one of the following factors which are outlined in Section 2202(a)(4)(A)(ii) of the CARES Act:

The Act defines a CRD as:

is diagnosed with COVID-19, with a CDC-approved test;

whose spouse or dependent is diagnosed with COVID-19, with a CDC-approved test;

who experiences adverse financial consequences as a result of being quarantined, furloughed, laid off, having work hours reduced, being unable to work due to lack of child care due to COVID-19, closing or reducing hours of a business owned or operated by the individual due to COVID-19; or

other factors as determined by the Treasury Secretary.

Individuals are permitted to pay tax on the income from the hardship distributions over a three-year period.

Individuals may choose to repay hardship distribution amounts back to the plan over the next three years.

The repayments do not count toward the annual retirement account contribution limits.

The solo 401k trustee, not the solo 401k plan provider, will need to retain records of eligibility. However, the solo 401k plan provider will prepare the participant loan documents, the distribution form and issue the required Form 1099-R for the qualifying distribution.

Solo 401k Required Minimum Distributions

Have requirement minimum distributions from solo 401k plans been delayed?

Yes, the legislation waives the requirement for any RMD from a solo 401k plan that is required to be paid in 2020. This includes 2019 RMDs having a required beginning date of April 1, 2020.

If your already made your solo 401k RMD in 2020, then you may roll it back into the solo 401k plan or to a Traditional IRA.

For example, Ben turned turned 70 1/2 in 2019, so his first RMD would be due by April 1, 2020.

Ben did not take the distribution in 2019 but instead is waiting to take it by April 1, 2020. However, because of the CARES Act, Ben is not required to take his 2019 RMD by April 1, 202o. Ben is also not required to take the 2020 RMD by December 31, 2020.

If Ben did take his first RMD (the 2019) by April 1, 2020, it is subject to the waiver for 2020 and the amount can be rolled over to a Traditional IRA or back to the solo 401k plan.

However, if Ben took his 2019 RMD in 2019, he cannot roll it over to an IRA or back to the solo 401k plan.

IMPORTANT: Until the IRS releases more guidance, if you took an RMD from your solo 401k plan between February 1 and May 15, 2020, you have until July 15, 2020 to roll over the RMD payment back to the solo 401k plan or to an IRA. However, if you took the RMD in January 2020 and after May 15, 2020, you have 60 days from the date the distribution was received to roll it over to an IRA or back to the solo 401k plan.

Does the RMD waiver also apply to inherited IRAs and solo 401k plans?

Yes, the waiver also applies to both inherited IRA and inherited solo 401k funds, so RMDs are not required in 2020 from beneficiary accounts either.

Does the RMD waiver only apply to full-time employer plans?

The 2020 RMD waiver applies to both full-time employer plans as well as self-employed plans for owner-only businesses such as solo 401k plans, SEP IRAs and SIMPLE IRAs.

If I don't take the RMD in 2020, will I have to take it in 2021?

No, the 2020 RMD will not need to be made up in 2021, so just the 2021 RMD will apply in 2021.

If I want, can I still take the 2020 RMD?

yes, and taxes would apply.

Do I have to be affected by COVID-19 in order to have my RMD waived?

No. It automatically applies to everyone who is subject to RMDs from solo 401k plans and IRAs.