Last Updated on December 8, 2025

Depending on what stage you are in the solo 401k process, you basically need to be aware of the following 4 important solo 401k deadlines:

- Solo 401k Contribution Deadline

- Solo 401k Establishment Deadline

- Solo 401k Loan Payment Deadline

- Solo 401k Form 5500-EZ Filing Deadline

- Solo 401k Form 1099-R Filing Deadline

Solo 401k Contribution Deadline

Contributions to a Solo 401k plan must be made by your business tax return due date plus extensions.

The self-directed 401k contribution deadlines are driven by the type of entity sponsoring the self-directed solo 401k.

Following are the Year 2025 Solo 401k Contribution Deadlines

- If the entity type is a Sole Proprietorship, the annual solo 401k contribution deadline is April 15, or October 15 if tax return extension is filed.

- If the entity type is an LLC taxed as an S-Corporation (calendar year), the annual solo 401k contribution deadline is March 16, or September 15 if tax return extension is filed.

- If the entity type is an LLC taxed as a Partnership (calendar year), the annual solo 401k contribution deadline is March 16, or September 15 if tax return extension is filed.

- If the entity type is an LLC taxed as a Sole Proprietorship, the annual solo 401k contribution deadline is April 15, or October 15 if tax return extension is filed.

- If the entity type is a Partnership (calendar year), the annual solo 401k contribution deadline is March 16, or September 15 if tax return extension is filed.

- If the entity type is an S-Corporation (calendar year), the annual solo 401k contribution deadline is March 16, or September 15 if tax return extension is filed.

- If the entity type is an C-Corporation (calendar year), the annual solo 401k contribution deadline is April 15, or October 15 if tax return extension is filed.

Example

John Doe’s self-employed business is a calendar year S-corporation having a tax filing deadline of March 16, 2026; however, John timely files tax return extension, so he has until September 15, 2026 to make his Solo 401k contributions (both employee and employer).

IMPORTANT

The annual solo 401k contribution limits as affected by the type of entity sponsoring the solo 401k plan.

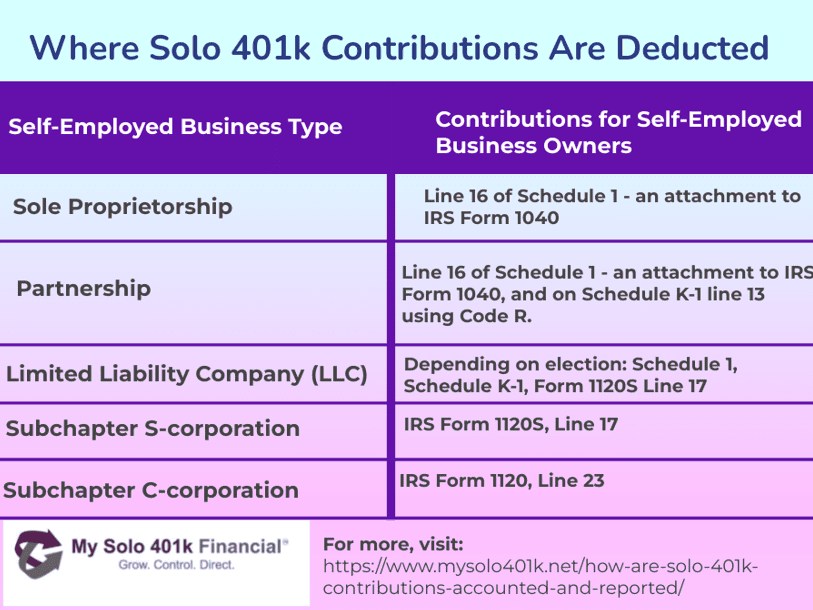

- If the entity type is a Sole Proprietor, the starting figure for calculating the annual solo 401k contribution is line 16 of Schedule 1- an attachment to IRS Form 1040.

- If the entity type is a C-Corporation, the starting figure for calculating the annual solo 401k contribution is W-2 income.

- If the entity type is an S-Corporation, the starting figure for calculating the annual solo 401k contribution is W-2 income.

- If the entity type is a Partnership, the starting figure for calculating the annual solo 401k contribution is line 16 of schedule 1 – an attachment to IRS Form 1040, and on Schedule K-1 line 13 using Code R.

The 2025 Solo 401k Establishment Deadline

Self-employed individuals planning to save on taxes for the 2025 tax year, a self-directed solo 401k is a good option. However, time may be running out in order to preserve the right to make both employee and employer contributions. Reason being, unlike a SEP IRA which only accepts employer contributions (aka profit sharing contributions), a solo 401k allows for both employee and employer contributions. However, in order to allow for more time to make employee contributions to the solo 401k the solo 401k must be established/adopted by December 31, 2025. A solo 401k will meet the establishment deadline for 2025 for making employee (pretax and Roth) contributions as long as the solo 401k plan documents are signed by 12/31/2025.

Sole Proprietorship or a LLC taxed as a Sole Proprietorship

Also, for a business taxed as a sole proprietorship, the solo 401k setup deadline can be confusing. Visit here to learn more about the solo 401k setup deadlines for a sole proprietorship or an LLC taxed as a sole proprietorship.

Example 1: Ben is a sole proprietor with a law practice. In February 2026, Ben decides to open a solo 401k retroactively for 2025. Provided the solo 401k plan is opened by April 15, 2026 (his 2025 tax filing, without extensions), Ben will be able to fund the plan with both 2025 employee contributions and employer contributions. Note that he can also wait to make the 2025 solo 401k employer contributions by October 15, 2026.

Example 2: Same example as above, Ben is a sole proprietor and in June of 2026 he decides to open a solo 401k retroactively for 2025. As long as the solo 401k plan is opened by October 15, 2026 (his 2025 tax filing deadline with extension), Ben will be able to fund the plan with only 2025 employer contributions. However, he won’t be able to make employee contributions.

Setting Every Community Up for Retirement Enhancement (SECURE) Act Impact on the Solo 401k Setup Deadline

The SECURE Act changed the solo 401k setup deadline but it caused confusion because the new rules pertaining to the deadline to establish a solo 401k plan only changed for making profit sharing (aka employer contributions) not employee pretax or Roth contributions (aka salary deferral contributions). As a result, if a solo 401k is adopted by December 31, 2025, the self-employed business owner will be able to make both employee and employer contributions for 2025 in 2026 by his or her business tax return due date including business tax return extensions.

If the solo 401k is not adopted until January 1, 2026 or after but by the self-employed business tax return including the business tax return extension deadline, the business owner can at minimum make employer profit sharing contributions as well as voluntary after-tax solo 401k contributions.

Solo 401k Loan Payment Deadline

Solo 401k loan payments are due either monthly or quarterly, determined at time of initial Solo 401k loan issuance. However, a grace period is available for missed payment. The grace period calls for the late payment to be made by the last day of the quarter (3 month) following the quarter in which the loan payment was due.

Example: On January 23 Jane Doe processed a Solo 401k loan amount of $20,000 having 15 year term. Since Jane is using the borrowed funds towards the purchase of her primary residence, the Solo 401k participant loan can exceed the standard 5 year period. Further, Solo 401k loan is payable monthly with the first fixed loan payment amount of $370 due on February 23. Therefore, if Jane is unable to make her scheduled loan payment by the February 23 due date, which is the first quarter, Jane must make the missed payment by June 30, which is the last day of the quarter following the quarter in which the missed loan payment was due.

Solo 401k Form 5500-EZ Filing Deadline

The Solo 401k business owner may have to file an annual return/report form by the last day of the 7th month after the Solo 401k plan year ends. Form 5500-EZ is used by the self-employed business owner to report on a yearly basis the total value of the Solo 401k plan; however, Form 5500-EZ does not need to be filed until the Solo 401k plan total assets exceed $250,000. Lastly, all Solo 401k Plans must file a Form 5500-EZ for the final plan year to show that all plan assets have been distributed. CLICK HERE to read our FAQ page on Form 5500-EZ.

Solo 401k Form 1099-R Filing Deadline

Anytime a plan participant or beneficiary takes a distribution from his or her self-directed solo 401k, IRS reporting requirements apply. 1099-R reporting also applies to in-plan Roth 401k conversions. Payers must send a Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc., to the IRS and to the individual receiving the distribution. The form is due to the IRS by February 28.