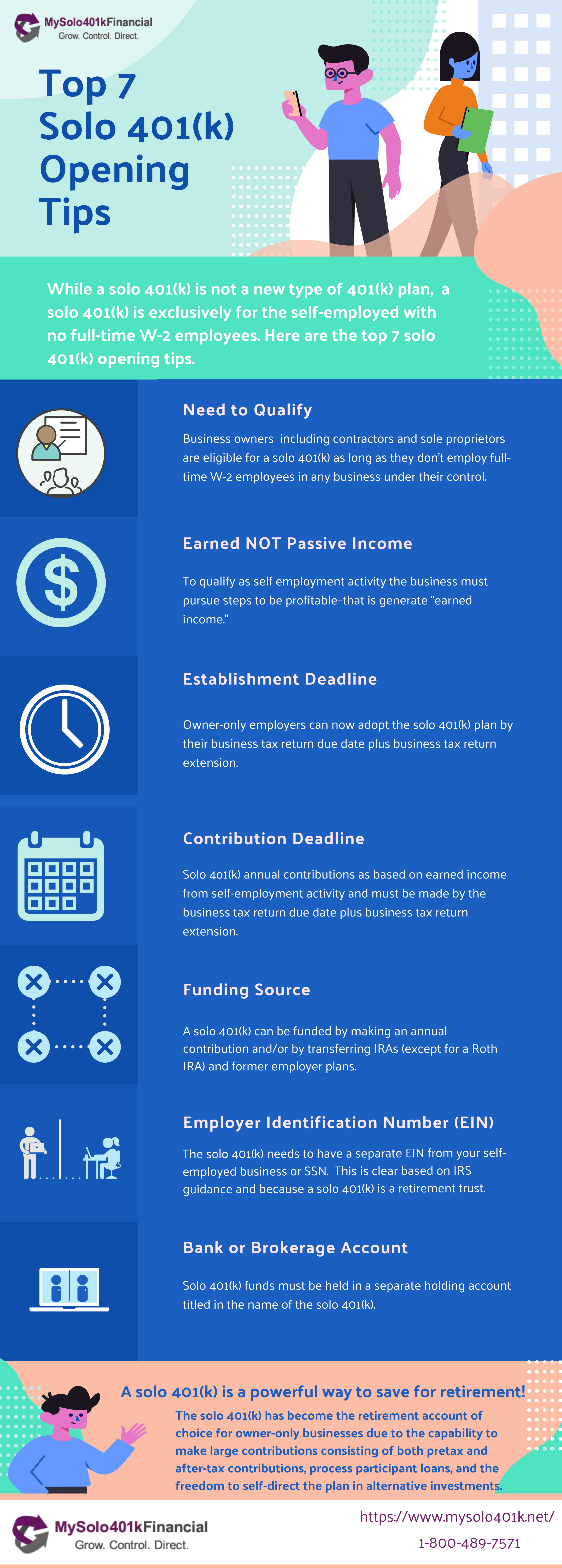

Last Updated: December 18, 2022

The solo 401k plan, commonly referred to as a self-directed Solo 401k because it allows for a variety of investment types is the retirement plan of choice for the self-employed or owner-only businesses for the reasons listed below.

401(k)/Profit-sharing plan for your business

For 2022, the solo 401k plan allows you to stash away money tax-deferred or tax-free (Roth Solo 401k or Voluntary After-Tax) up to $61,000 or $67,500 for those age 50 or over.

Unlimited investment options

Put your hard-earned money to work! At no additional charge, you can choose a bank or brokerage account to establish a checking account for your Solo 401k for use in making alternative investments such as real estate, cryptocurrency, private investments, private loans, etc. by simply writing a check, or by wire.

As part of our services, we would guide you through the process to set up an account for your Solo 401k. You can have a bank or brokerage account for your solo 401(k), or even both (and we would help you set up the accounts as part of our services). For example, if you wish to have an account at a brokerage like Fidelity or Schwab, we would prepare all of the paperwork that Fidelity or Schwab needs to set up a free account for the Solo 401k (i.e. no set up or maintenance fees) that comes with a free checkbook and through which you can invest in traditional investments (e.g., stocks, mutual funds, bonds, etc.) as well as alternative investments such as real estate, cryptocurrency, promissory notes, etc. since they are allowed under our IRS-approved plan documents. Please see more at the following links:

High Contribution Limits

SEP IRA contribution limit is only 25% of employee compensation and does not permit elective deferrals or catch-up contributions. On the other hand, a Solo 401k allows for all three plus elective deferrals of $20,500 (for 2022), which can be applied as Roth Solo 401k contributions. Note that the catch-up contribution of $6,500 (for 2022) can also be applied as a Roth Solo 401k contribution, thus allowing for Roth Solo 401k benefit contributions of $27,000. In order to make the catch-up contribution you must be age 50 or older by the end of the year for which the contribution is applied for.

Solo 401k Participant Loan Option

The solo 401k allows for participant loans, and the solo 401k loan document preparation is included in our fees.

Participants loans are essential for growing companies.

The maximum amount that the Solo 401k plan can permit as a loan is (1) 50% of your vested account balance, or (2) $50,000, whichever is less.

For example, if a participant has an account balance of $60,000, the maximum amount that he or she can borrow from the account is $30,000.

The personal 401k loan option is available to each Solo 401k participant, and the loan limit is 50% of the account value not to exceed $50,000. For example, John and Jane, who live in Washington, both participate in the JJ Solo 401k Plan and both want to process a loan (borrow) from their Solo 401k. Jane’s Solo 401k current balance including non-liquid assets is $120,000 and John’s is $60,000. Jane can borrow up to the maximum amount of $50,000; and John can borrow $30,000. The reason John’s loan benefit is less is because the loan rules only permit the participant to borrow 50% of his solo 401k account balance not or $50,000, whichever is less. Lastly, John and Jane can use the loan proceeds for any purpose including purchasing a vacation home in Vancouver WA.

Business Funding or Investment

Each Solo 401k participant can borrow up to $50,000 for any purpose including to fund or inject funds into a business or make an investment.

Hardship withdrawal choice

The solo 401k plan gives you the option to withdraw from your Solo 401k under certain conditions, should you find yourself in financial hardship. To learn more about the hardship distribution rules, VISIT HERE.

Compliance-approved plan documents

You will also receive plan documents, which are compliant with government regulations, and IRS Determination letter confirming that this is a 401k plan that meets the requirements of a qualified plan .

Power to amplify tax-deductible contributions

Amplify your tax-deductible contributions through your Solo 401k, up to $61,000, or $67,500 if age 50 or older in 2022.

Solo 401k Allows for All Three Contribution Sources

The solo 401k offered by My Solo 401k Financial allows for all three contribution sources (i.e., pretax, roth and voluntary after-tax). The rules require each source to be separately tracked. We would of course assist with the set up of the bank/ brokerage accounts which is covered in our pricing. The following pages cover the differences and similarities between each source. https://www.

Straightforward and Inexpensive to Administer

A Solo 401k is not subject to Form 5498 reporting like SIMPLE and SEP IRAs. Further, unlike all IRAs, the Solo 401k IRS rules allow for the self-employed business owner to serve as Trustee of his or her Solo 401k, hence why you can safe keep the alternative investment paperwork instead of paying a custodian like Pensco Trust, Equity Trust or Entrust to safe keep the investments. Lastly, a Solo 401k does not require filing of tax forms unless: you make distributions, process conversions or the total Solo 401k account value exceeds $250,000, with the former requiring filing for Form 1099-R to report the distributions and conversions and the latter requiring issuance of a Form 5500-EZ.

Form 5500-EZ Preparation

If your account exceeds $250,000, we can prepare your Form 5500-EZ at no additional cost.

Form 1099-R Filing

Distributions from the solo 401k plan must be reported on Form 1099-R. We prepare this form on your behalf at no additional cost.

Exemption from UDFI

Unlike IRAs, solo 401k plans are exempt from paying unrelated debt financed income tax (UDFI) which is a tax that applies to IRAs that utilize debt financing (non-recourse loan) for use in investing in real estate.

Great for Consolidating SEP, SIMPLE, Traditional IRA and all Qualified Plans

Not widely known, Solo 401k can be used to consolidate all of your retirement accounts including former employer plans such as 401k, 403b, Defined Benefit as well as government plans such as 457b and Thrift Savings Plans, provided you meet the Solo 401k qualification requirements: you are self-employed with not full-time employees.

Solo 401k Questions

LLC that Hires Employees:

The solo 401k establishment process.

For Video Slides, CLICK HERE.