Recent ROBS 401K Program Webinars:

- Use 401k/IRA to Buy a Business

- Top Franchise Funding Considerations

- “How to” Exit a ROBS 401K Business Financing Plan

- Top ROBS C-corporation FAQs w/ Tax Expert Familiar with ROBS 401K Structure

- Rollover as Business Startup (ROBS 401k) PROS and CONS

Click HERE to learn how we can charge over $3500 less in the first-year alone for our ROBS Program

- Full-Service ROBS 401K

- 100s of 5-star Reviews

- ZERO negative reviews

About ROBS 401k Business Financing

What are the advantages using a ROBS 401k plan to finance my business as compared to traditional small business financing options?

Most aspiring or existing business owners looking for financing for their business consider just two options: borrow funds or sell an ownership stake in their business. Another option that may be available is referred to as a rollover as business startup (ROBS) plan that allows the entrepreneur to use his or her 401k, IRA or other retirement funds to finance the business.

There are several important differences between ROBS and traditional small business financing options:

Read more >>

What does the IRS say about rollover as business startup transactions?

To learn more about what the Internal Revenue Service has said Read more>>

Eligibility

Can I use my 401k, IRA or other retirement funds to buy or start a business or franchise?

We are often asked if 401k, IRA or other retirement funds can be used to buy or start a business or franchise.

The great news is that you can! While one option is to take a loan from your retirement account, there is another option (often called a rollover as business startup) that is more flexible and offers many benefits over a loan in providing funding to your franchise or small business startup. Read more>>

I'm still employed, so can I use my existing 401k funds to fund my start-up company?

I called my employer and spoke to someone in the HR Department and they said that I can’t use funds in my 401k to fund start up business or in any investment outside the mutual funds offered under the employer 401k plan. Are they allowed to do this? Read more>>

Can I invest funds in my 401a, 403b, 457 or government plan in my business start up?

Yes a 401A, a type of governmental plan offered to employees of the USA or governmental agency, or state government or political subdivision, may be transferred to a ROBS 401k. Read more>>

What are the 457b differences and which can be transferred to the business financing 401k (ROBS)?

There are two types of 457(b) plans but only one can be transferred to a 401k such as the business financing 401k plan. The first type is a Tax-Exempt 457(b) which is the type that cannot be transferred to the business financing 401k (ROBS) or to an IRA. The second type is a Governmental 457(b) and this type can be transferred to the ROBS 401k plan. To learn more about these types of 457(b) plans CLICK HERE.

Does my the C-Corp have to be my new business, or can it exist as a shareholder of a separate business? My partners do not want to be a C-Corp. I imagined a scenario where I could form a C-Corp and somehow make it a parent or child of the main organization.

The C-corporation needs to own and operate the business. The C-corporation can do this through a subsidiary that the other investors invest in provided that the C-corporation is the majority owner of the subsidiary LLC and the other owners receive an ownership interest proportional to the funds invested.

Can I use my 401k to start a real estate operating company?

If your objective is to invest in real estate via a rollover as business startup transaction, you could do so by funding a c-corporation that operates as a real estate operating company. In order to qualify as a real estate operating company, a at least half of the assets of the corporation must be invested in real estate which is managed or developed and with respect to which such corporation has the right to substantially participate directly in the management or development activities. Moreover, the entity in the ordinary course of its business must be engaged directly in real estate management or development activities. Furthermore, expenses related to the real estate must be paid by the corporation and the real estate cannot be used for personal use.

I plan on using my 401k start a business. I have lined up another investor who wishes to use retirement funds but will not be involved in the day-to-day operations of the business. Can he invest via a rollover business startup?

A ROBS 401k is not designed for someone who wishes to passively invest in a business. In order to participate in the 401k, the individual would need to be an employee of the business. While the investor would therefore not be able to invest his retirement funds in your business via our 401k Business Financing plan, he could invest in your business via our self-directed IRA LLC. The investment could be structured as debt (i.e. a loan to your business) or equity (i.e., the LLC purchases stock in your business).

I plan on using your 401k business funding services to buy a business (i.e. FedEx route) and would like to buy equipment for the business from my father. Is this allowed?

It is the opinion of the regulators that a “prohibited transaction” occurs when a 401k plan invests in a corporation where you expect that the corporation will enter into a transaction with a “disqualified person." Family members who are disqualified persons include a spouse, ancestor, lineal descendant, or any spouse of a lineal descendant (see more). As such, the company should not buy equipment from your father (who is an ancestor) or your son (who is a lineal descendant). While other family members may not technically be a disqualified person such that you could make a reasonable business decision for the company to purchase equipment from such other family members, it would be prudent to obtain and retain documentation demonstrating that such a transaction was at fair-market value.

I have a former employer plan that I am looking to use to buy a franchise with my husband. While we will both work full-time in the new business, my husband will also continue to work part-time at his current job. He has a 401k through his current employer. Is it possible to rollover his balance into the business 401k if he remains employed?

If your husband wants to transfer funds from his current employer plan, he should check to see whether the plan allows him to rollover funds while still employed (an in-service transfer). Note that if he has funds in his current plan that were transferred from a prior employer plan the plan will typically allow him to transfer out those funds while still employed. If you would like us to review the plan, we would be happy to do so please just request the summary plan description and then email it to us.

While I am seriously considering using a ROBS 401k to start a business, the tax implications are my main concern. Unlike an S-Corp or LLC funded with non-retirement money, the C-Corporation would be subject to corporate income taxes, so profits would be taxed twice. Is there no other alternative other than the C-Corp?

If you wish to fund your business via a rollover as business startup, the entity funded with your retirement funds must be a C-corporation. While it certainly true that business advisers will generally recommend an LLC/S-Corp over a C-Corp there are certain advantages of a C-corporation (see for example, the advantage discussed in the following article: http://www.legalzoom.com/incorporationguide/corporatetaxadvantage.html).

As a general matter, those advisers will recommend an LLC/S-Corp because of the perception that C-Corporations are subject to a "double tax" (where the "double tax" refers to the fact that the corporation must pay tax on its income and any corporate profits distributed to the stockholders are subject to capital gains tax). While this may be generally true, it is worth noting that with respect to our 401k Business Financing plan (i) any double taxation effect is mitigated by the fact that any dividends paid with respect to the stock held in your 401k will paid to your 401k on a tax-deferred basis; and (ii) any taxable income at the corporate level can be reduced by a reasonable salary paid to you as an employee of the corporation (since this would be an expense to the corporation). Of course, when you withdraw funds from your 401k, those funds will be considered income subject to income taxes (and possibly penalties) in the year of the distribution. It is worth noting that the withdrawal may be years later (e.g., when you retire) and you may be in a lower income tax bracket.

Ultimately, if you want to use your retirement funds to finance the business the business must be organized as a C-corporation. As such, perhaps a better comparison would be (i) the cost to access to your retirement funds, vs. (ii) the cost to obtain other types of financing or the cost to simply withdraw the money from your retirement account and pay the applicable taxes and penalties. For example, consider the costs of our plan vs. a $100,000 loan with a 7 year term at an interest rate of 7%. With our plan, our setup fee and annual fee over 7 years will total $7,000 plus an additional estimated costs of $4000 for annual valuations and if needed premiums for a fidelity bond (estimated total: $11,000). With the loan, you would pay over $26,000 in interest (see calculator at https://smallbusiness.yahoo.com/advisor/businesstools/loancalculator). If you simply withdraw the money from your retirement account you will have to pay a 10% penalty as well as income taxes on the withdrawn amount (perhaps $35K or more).

Funding Your Business

Your website mentions you use C Corp structure. Any restrictions to B Corporations?

We understand that by "B Corporation" you a referring to a type of corporation that is authorized in certain states which are allowed to have a purpose other than generating profit for the shareholders. This type of corporation is not compatible with a ROBS business financing 401k transaction as you are investing your retirement funds to grow your retirement account (i.e. generate profit).

If fund my business with the 401k Business Financing plan will My Solo 401k Financial you hold the rollover funds?

No. To ensure that your business is financed as fast as possible we will fully assist you with the rollover of your retirement funds through the 401k Business Financing Plan. However, we will never hold your money.

How can I rollover my IRA funds to the 401k Business Financing Plan?

As long as you are rolling over funds from an eligible IRA (only Roth IRA funds are not eligible), there are two ways to move IRA funds to a ROBS 401k business financing vehicle.

Option 1: Via a Direct Rollover:

When funds are directly rolled over from IRAs to a 401k for business financing, the check is made payable in the name of the 401k or directly deposited electronically into the 401k account. This is the preferred method of moving funds from an IRA to a 401k because it is reported by the releasing financial institution holding the IRA funds on Form 1099-R using a code “G” in box 7 that communicates to the IRS the IRA funds were directly deposited into a 401k. Read more>>

Can I receive a salary from my new business?

Yes. You are required to be an employee of your new business that is financed with the 401k Business Financing Plan. While you are not legally required to take a salary you may take a reasonable salary once the business generates revenue.

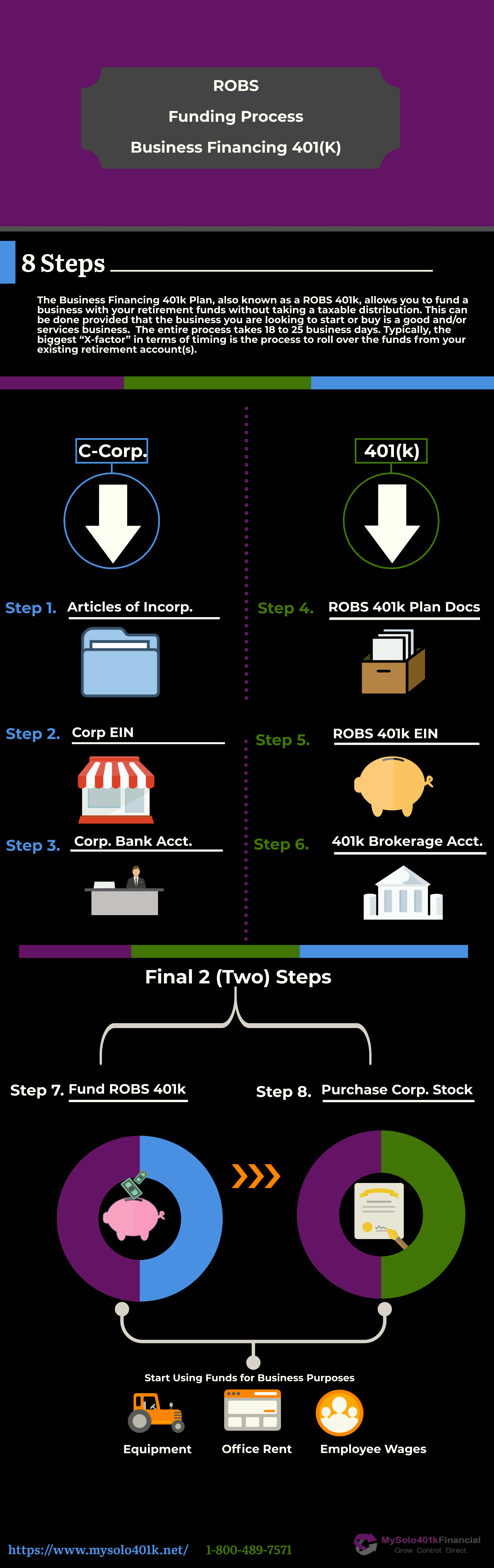

How long does the process take?

While the required time will vary, the 401k business financing process generally takes 2-3 weeks. Typically, the biggest source of any delay will be on the part of your current retirement account provider in rolling over your retirement funds to your new 401k account. Read more>>

I am considering using the 401k Business Financing plan to buy a franchise. Does My Solo 401k pay referral fees to franchise promoters?

While many companies pay significant (and often undisclosed) referral fees to franchise promoters or other business brokers, My Solo 401k Financial’s policy is not to pay referral fees in connection with the 401k small business financing retirement arrangement (401k Business Financing Plan). Not only is the payment of referral fees questionable from an ethical and legal perspective, it Read more >>

Can I pay My Solo 401k Financial's fees with the proceeds of the 401k business financing transaction?

In its 2008 guidance regarding ROBS Business Financing, the IRS flagged the payment of fees as a potential prohibited transaction. In particular, the IRS stated that a prohibited transaction may occur where immediately after being funded via a ROBS transaction a corporation pays the professional fees of the ROBS facilitator out of the proceeds of the funding transaction. For this reason Read more>>

Do I have to invest personal funds in the new company?

If you employ a 401k Business Funding strategy to finance your new company, you are not required to invest any of your personal funds (i.e. money outside of your retirement account). However if the 401k owns 100% of the stock of the corporation, the assets of the corporation will be considered assets of the 401k plan under the Department of Labor’s Plan Asset Rules. In that case, Read more>>

Can I pay off my credit card that I used to pay for startup business expenses?

After you invest your retirement funds in your business, you should not pay off your credit card with funds from your business account. Paying off your personal debt with funds in your business account could be challenged as a prohibited transaction. While you should not use funds in the business bank account to pay off the credit, there is another option to use your retirement funds to payoff your credit card.

Our 401k Business Financing plan allows you to take a participant loan from the 401k funds that are not invested in the company. You could take a loan of up 50% of the amount of retirement funds that you transfer into the new 401k from your existing retirement account (not to exceed $50,000). You could use the proceeds of the loan to pay off your credit card, for personal living expenses, etc. It will be important to document the loan and we handle the required loan documents as part of our services. You would pay the loan back to the 401k account in monthly/quarterly payments of principal and interest at prime plus 1% over a 5 year term.

While you should not pay off your credit card with funds from your business account, the corporation could issue stock to you personally as consideration for paying the reasonable and legitimate business expenses with your credit card.

Can I be reimbursed for startup business expenses that I have paid with personal funds?

You should not be reimbursed for business expenses paid with personal funds by the corporation that is funded with your retirement funds via our 401k Business Financing plan. This reimbursement could be challenged as a prohibited transaction and/or an attempt to circumvent the distribution rules. Instead, such an amount could be considered part of your personal investment in the business. As a result, you would personally receive stock in the corporation in exchange for paying the reasonable and legitimate business expenses on behalf of the corporation. Going forward, it is a good practice for all businesses (including those that were not funded with 401k, IRA or other retirement funds) to pay for business expenses from the business account rather than using personal funds.

Do I have to invest all of my retirement funds in the business at the same time?

You can choose to invest your retirement funds in your business at one time or in a series of investments. For example, you may need funds now for an initial capital investment (e.g., real estate purchase and build out) and additional funds at a later (e.g., for inventory, marketing, operating expenses, etc.). Our 401k Business Financing plan allows you to invest your retirement funds in your business at one time or a series of investments. If you make additional investments of your retirement funds, you would do so by purchasing additional stock in your corporation. The stock will be issued at fair market value which should be supported by a business valuation. Moreover, other employers participating in the 401k should be notified of the opportunity to use their retirement funds to purchase company stock.

Do I have to open my business bank account at a particular bank?

You can open the bank account for your business at the bank of your choosing. This is the account where your retirement funds will ultimately be deposited as part our 401k Business Financing process. While you are free to choose your bank, it is prudent to choose carefully. A bank that may be a good fit for one business may not be the best choice for another type of business. Important considerations may include relationship with your banker, fees, online access, size, willingness to lend, and specialized lending among others.

Where are my retirement funds transferred to? Where is my 401k account at?

When you use your 401k for business financing, the funds may not be transferred directly to you or your business. Instead, your retirement funds must be transferred to a new 401k plan sponsored by your business. These funds are transferred as a direct rollover, trustee-to-trustee transfer or rollover in order to avoid triggering tax or penalties. While the 401k account may be at a bank or a brokerage, it is typically best to open the account a brokerage firm (e.g., Fidelity Investments). First, the brokerage account will have a variety of investment options for the funds that you don’t invest in the business including mutual funds, stocks, bonds, ETFs, and FDIC-insured CDs. Moreover, in the event that your employees want to participate in the 401k plan it will be easy to setup those employees with accounts where the employee can invest his or her retirement savings. As part of our ongoing compliance support, we will establish a brokerage account for your employees just as we do for you at the beginning of the 401k Business Financing process. Please note that we will never have access to the retirement funds of you or your employees.

What is the role of the brokerage firm holding the 401k account? How much do they charge?

The IRS rules require that your 401k account be at a financial institution such as a bank or a brokerage. For our 401k Business Financing plan, the account is typically established at brokerage firm (e.g, Fidelity Investments). The role of the brokerage firm is to simply act as the custodian of the account. As such, the firm will not perform any record-keeping and tax reporting services. Given that we are the 401k plan provider rather than the brokerage firm it will important to contact us with any questions with respect to your plan (e.g, if you wish to take a loan, distribution, etc.). Please note that the brokerage firm does not charge a fee that is a percentage of the funds in the account. Instead the firm simply charges transaction fees such as a wire transfer fee to wire the funds that you use to fund your business to your corporate bank account or a commission if you purchase publicly-traded stock (e.g., Apple, Google, etc.) with some of the funds that are not invested in your business.

What happens to the money that I don’t invest in the business?

As we guide you through the steps in the rollover as business startup process, your retirement funds will first be transferred tax and penalty-free to a new 401k plan sponsored by your business. While our IRS-approved plan will allow you to invest in your own business, you are not required to invest all of your retirement money in your business. The funds that are not used for business financing will remain in your 401k account which will typically be at a brokerage firm. By having your account at brokerage firm you will have numerous options to invest your remaining 401k funds that are not used to finance your business including the option to invest in mutual funds, stocks, bonds, ETFs, and FDIC-insured CDs.

I assume the tax ID's and other applicable info needs to be setup prior to opening a business account, right?

That is correct. We will first form a C Corporation and then once the articles are issued by the Secretary of State will obtain an employer identification number from the IRS for the C Corporation. You will need both to open a bank account (and may need additional documents depending on the bank such as a corporate resolution which we can provide as part of our services).

I am using about half of my 401k to start a business (i.e. child care/educational franchise). Can I invest the rest of my retirement funds in real estate, precious metals and other alternative investments?

Yes. Our 401k Business Financing plan allows you to invest any retirement funds that are not being used for business financing in alternative investments. For example, you could purchase a rental real estate property, invest in promissory notes, buy precious metals, etc.

You would make the real estate and other alternative investments via the 401k rather than via the C-corporation where the proceeds of the real estate and other investments would flow back to the 401k and grow on a tax-deferred basis. There are certain limitations that would apply including that you would not be able to work on the properties (e.g., no "sweat equity"), all income and expenses would flow in and out of the 401k account, no personal use of the property, etc. For more on investing in real estate via your 401k, please see the following page (note: even though the page refers to a Solo 401k, the same principles apply to investing in real estate via your 401k): https://www.mysolo401k.net/solo-401k-real-estate-investment-procedure/

In addition, your 401k account will be at a brokerage firm that will allow you to invest in a full range of traditional investments such as mutual funds, stocks, bonds, ETFs, and FDIC-insured CDs. This will allow you to fully diversify your retirement funds and manage risk across your investment portfolio.

Ongoing Compliance

I am worry about years when profits are low, so how frequently can salaries be adjusted?

The salary can be adjusted as you see fit. The salary needs to be reasonable. This means you should wait to receive w-2 compensation (e.g., salary, bonuses, etc.) until the C-corporation is generating income to justify your salary and then your salary should not be unreasonably high (i.e., no more than what the company would have to pay someone else to do all of the things that you do). Any compensation that you receive should be paid to you as W-2 wages (i.e. not as 1099 income). As such, it will be prudent to coordinate with your business tax adviser.

Do I have to make salary contributions to my 401k profit sharing plan?

If you use a ROBS business financing strategy to fund your franchise or other small business, your company will have a 401k. You should defer at least 1% of your salary into the 401k and may defer up to the federal maximums. Read more>>

Can my employees participate in the company's 401k?

If you use a 401k business funding strategy to fund your existing franchise or other small business, your company will need to adopt a 401k. Any other full-time employees must be given an opportunity to participate in the plan including rolling over retirement funds into the 401k, and if they elect to do so, Read more>>

Do I need to obtain an annual appraisal of my business?

If you use a 401k small business financing strategy to fund your new franchise or other small business start-up, your business will need to sponsor a 401k profit sharing plan. In order to maintain the compliance of the plan the value of the plan assets (including the value of the company stock held in the 401k) will need to be reported each year. Read more>>

Does a Form 5500 need to be filed for my company's 401k?

In its 2010 guidance, the IRS reported common ROBS operational mistakes made by new business owners using their retirement funds to pay business start-up costs (see here). The IRS noted a common misunderstanding that a Form 5500 is not required to be filed if the business is only owned by an individual and his or her spouse. In the referenced guidance, Read more>>

Can I rollover additional retirement funds in the future?

If your retirement funds are eligible to be rolled over to a qualified plan, our 401k Business Financing plan will allow you to transfer additional retirement funds to the plan. To facilitate that process, please (1) provide us the most recent account statement for the retirement account from which you wish to rollover additional funds and (2) contact the administrator of such account and ask for their transfer out paperwork and then forward to us for completion (note: if the account is an IRA account they may state that the transfer paperwork must be provided by the receiving financial institution in which case we will use our internal form).

If you wish to invest these funds in your business, you would do so by purchasing additional stock in your corporation. The subsequent stock purchase should be at at fair market value as supported by a business valuation. In addition, the stock offering should be made available to other employers participating in the 401k.

I used my 401k to open a franchise. My business is successful and generating significant revenue. How can I get money out of the business?

You may receive reasonable w-2 compensation (e.g., salary, bonuses, etc.) if your business is generating income to justify your compensation. Your compensation should not be unreasonably high. In determining what constitutes reasonable compensation, you should consider what your business would have to pay someone else to do all of the things that you do (for more on what constitutes a reasonable salary click here >>). Besides paying you reasonable compensation, the corporation could elect to distribute profits to the owners (i.e., dividends to the stockholders). If the corporation decides to distribute profits to the stockholders, the profits must be allocated based on the ownership percentages. This means that some of the profits will go back to the brokerage account for your 401k. Profits that go back to your 401k will grow on a tax-deferred basis and may then be invested via your brokerage account (e.g., in mutual funds, equities, ETFs, etc.).

I left Corporate America to start my own business in a completely unrelated field (i.e., fast casual franchise). I have made over $200K per year for the last 5 years and am worth at least that much money. My business is successful and generating significant revenue. Can I receive the same salary in my new venture?

You may draw a reasonable salary for the work that you perform for the franchise operation. In considering the question of what constitutes a reasonable salary, the courts and regulators have weighed many factors including the market rate for the work that you are performing (i.e., what your franchise would need to pay someone else to perform the same tasks). One factor that is not relevant to the analysis is the salary that you have received in previous unrelated positions. For example, consider a person who leaves her successful position as a securities litigation attorney that paid her a very high salary to open a cupcake franchise. The fact that she received significant compensation for her previous attorney position will not justify the cupcake franchise paying her the same salary.

I rolled over my 401k to buy a business. The business is doing well and I am receive a small salary. My personal expenses have gone up recently. Can I increase the salary that I receive from my business?

If you are receiving a nominal salary and your business is successful, you may increase your compensation provided that your total compensation is reasonable. An important factor in determining reasonable compensation is the amount that your business would have to pay an unrelated person to perform that tasks and duties for which you are responsible. For a discussion of additioanl factors, please click here >>. It is important to note that a factor that is not relevant to whether your compensation is reasonable is an increase in your personal expenses.

Do required minimum distributions (RMDs) apply to the business financing 401k plan?

Required minimum distribution requirements refers to the fact that when one reaches 70.5, he or she is required to start withdrawing funds from his or her retirement accounts(s). Such RMD requirements also apply to the ROBS 401k plan. As such, the amount of the required minimum distribution will need to be withdrawn from the 401k account. This amount could be funded with cash in the 401k account which could come from distributions of profit from the corporation, buyback of stock by the corporation, or contributions from your reasonable W-2 wages. In the event there is not enough cash in the ROBS 401k account, you could take an in-kind distribution of Company stock - in which case you would certainly need a valuation to be able to demonstrate that the amount of stock is equal to at least the amount of the required minimum distribution.

I used my 401k to start a business and my business has hired employees. When do I have to offer the 401k to my employees?

When you fund your business via a ROBS 401k, it is important to understand that the 401k plan is not just for you. Instead, the 401k plan is sponsored by a C-corporation. As an employee of the C-corporation, you may participate in the 401k. Other employees may also be given an opportunity to participate in the 401k if they are eligible. Employees will be typically be eligible if they are w-2 employees working at least 1000 hours per year and with 1 year of service. As part of our ongoing support for your 401k, we will assist you in offering the plan to employees and on-boarding those employees who wish to participate.

I have an employee who is eligible to participate in the 401k and wants to make contributions to her 401k. Where should she deposit her 401k contributions?

As your business or franchise grows and you hire w-2 employees, those employees will typically be eligible to participate in the 401k once they are working at least 1000 hours per year and with 1 year of service. The employees would need to be offered a chance to participate in the 401k. For those eligible employees who wish to participate in the 401k, a brokerage account would be established where the person could rollover funds and deposit 401k contributions as well as invest his or her retirement funds. As part of our ongoing support for your 401k, we will onboard those employees who wish to participate including establishing a brokerage account(s) for such employee(s).

Other Financing Options

I have $50K in a traditional IRA and would like to use it start a small business. Is there any option other than your 401k Business Financing plan?

If your business will not have any full-time employees you could rollover your money to a Solo 401k and then take a Solo 401k loan for business financing. You could take a loan of up 50% of the amount of retirement funds that you transfer into the Solo 401k from your existing retirement account (not to exceed $50,000). You could use the proceeds of the loan to startup your new business. It will be important to document the loan and we handle the required loan documents as part of our services. You would pay the loan back to the 401k account in monthly/quarterly payments of principal and interest at prime plus 1% over a 5 year term.

For a someone looking to start a small business with no employees, a Solo 401k may be a preferable option compared to a ROBS 401k. Since a Solo 401k is a one-participant plan, the compliance requirements are simplified relative to a ROBS 401k. As a result, the costs are also significantly lower (about 80% less). Moreover, your business entity does not have to be a C-corporation and can be an S-corporation, LLC or even a sole proprietorship.

Exit Strategies

Can I discontinue my 401k after I have completed the 401k business funding transaction?

For entrepreneurs using 401k funds to buy a business via a 401k business funding strategy, the franchise or other small business will need to adopt a 401k profit sharing plan. The Treasury regulations require that the plan be permanent (as opposed to a temporary) arrangement. These rules also generally provide that if a plan is discontinued within a few years after its adoption there is a presumption that it was not intended as a permanent program from its inception, unless Read more>>

I used my 401k to start a franchise. My business has grown and I have received several asset purchase offers which I am seriously considering. What is the mechanism to pull out my retirement funds when I sell my business?

If you sell your business via an asset sale, you could then dissolve the corporation which would mean that the corporation would have to pay off any outstanding debts and then the remaining funds would be distributed to the owners in accordance with the ownership percentages. As such, part of the funds would flow back to the 401k. Since the sponsor of the 401k (i.e., the corporation) would have been dissolved, the 401k would also have to be wound down and your funds would be transferred to an IRA. You could of course elect to withdraw funds from the IRA at that time and pay applicable taxes and possibly penalties.

If the 401k owns the company, can I purchase it back from the 401k by borrowing on the company once it is profitable and buying out the 401k and then putting the money into a standard program? If not, how do I ever get it where the business financing 401k can be bought out?

The buyback would entail the purchase of shares back from the 401k by the C-corporation (not you) using the after-tax profits earned in the business. Here are the steps for the C-Corporation buybacks from the ROBS 401k plan:

- As far as the mechanics of the buyback, the corporation would purchase the stock back from the 401k over one or a series of purchase provided that it would have to do so at fair market value at the time of each buyback.

- The value of the company stock will need to be supported by a third-party business valuation.

- The money would flow from the corporate bank account back to the 401k brokerage account on a tax-deferred basis.

Here is the impact on the ownership of the C-corporation:

- As the 401k sells stock back to the C-corporation, the number of shares held by the 401k will decrease. As a result, the 401k will own a lower percentage of the company.

- Conversely, the other owners of the business (i.e. you) will owner a greater percentage of the business.

- If the C-corporation buys back all of the stock from the 401k, you will no longer own company stock through the 401k and the other owner(s) will thus own 100% of the business

Here is how the price per share for the stock buyback is determined:

- The C-corporation must buyback the stock at fair market value.

- While the IRS doesn’t necessarily specify items that must be in the report, they have issued guidance on valuing a closely-held corporation (e.g., see IRS Revenue Ruling 59-60).

- Moreover, it is certainly a best practice if the valuation is prepared by a third party who is a business valuation specialist or someone who has relevant training and experience.

Here is what happens to the ROBS 401k:

- The proceeds of the stock buyback will be deposited in the 401k brokerage account & you can invest those funds however you see fit (e.g. stocks, bonds, mutual funds, etc.).

I’m trying to determine the tax consequences of a subsequent sale of the business, both as an asset sale and as a stock sale. I’m assuming any gain on sale would flow through to the 401k and be tax deferred unless/until I take distributions from that account and that any personal income tax impact would be minimal.?

In the event that you sell your ROBS 401k funded business you may sell the business as a stock or asset sale. It is important to note that this question should be posed to your business legal and tax advisers as there important tax and legal issues to consider. For example, in the event of an asset sale the gain is generally realized by the corporation. In the event of a stock sale, the gain is generally realized by the stockholders and in the case of any gain with respect to the stock held by the 401k any gain is tax-deferred. There would be additional 401k considerations - for example if you intend to terminate the 401k plan in connection with the sale.

MORE QUESTIONS

My early understanding of the ROBS model was I would not be able to draw a salary until the business was profitable, further investigation seems to show otherwise your thought on this would be appreciated.

Once the business that is funded with your retirement funds is generating income to justify your salary (not necessarily profit), you may receive reasonable compensation based on the work that you are performing which would be paid to you as W-2 wages.

Do you offer audit protection and if so, what are the details of your audit protection?

Our Guarantee provides that in the event of an Audit, we will step up as the Plan Provider to help you respond to the audit at no additional charge. Moreover, if the 401k Business Financing plan is challenged as prohibited transaction we will pay for legal counsel to represent you at no additional cost to you. See our Guarantee here: https://www.mysolo401k.net/401k-ira-business-funding-financing-guarantee/.

My account wasn't sure about this type of arrangement we have so he was asking if its possible to convert from a C corp to an S corp. From my understanding it was not because we needed to keep shares but I figured I would ask.

It is not possible as long as you own shares via the 401K. The Entity must be taxed as a C corporation.

How much is provided to us for taxes, do we need to do quarterly filings for a C Corp. Will this be provided with your service or do we get our accountant to do this?

As part of our ongoing compliance support for the business financing 401k plan, we will prepare the annual tax filing for the 401k (i.e. Form 5500). You will need to work with your business legal and/or tax adviser for licensing, tax, etc. requirements applicable to the C-corporation. We are happy to discuss with your accountant to answer any questions from a 401k perspective. Here are items to highlight for your adviser:

- The 401k funded business must be a C-Corporation and can NOT be an S corp

- Ownership will be via (i) 401k for your benefit and (ii) you personally in proportion to the funds invested

- Any compensation that you receive for the work performed needs to be paid as w-2 wages

- No personal loans to company

- No interact between this business and other businesses that you own

- Your only relationship should be w-2 employee and owner of the company.

Can employees who decline to participate in the business financing 401k plan later elect to participate in the plan?

The waiver would not be permanent (i.e. they would have the chance to participate in the future).

What’s considered a normal salary for 2 shareholders based off 150k profit a year company?

First, you are not entitled to receive a salary because you are an owner (shareholder). You are entitled to receive compensation for the work that you perform for the C-corporation that is funded with your retirement funds. You need to wait to receive w-2 compensation (e.g., salary, bonuses, etc.) until the C-corporation funded with your retirement funds is generating income to justify your salary and then your salary should not be unreasonably high (i.e., no more than what the company would have to pay someone else to do all of the things that you do). Please note that generally speaking the salary paid to you is independent of whether the company is generating a profit. For example, a business is obligated to pay its employees even if the business is losing money. Of course, companies may pay their employees a reasonable commission which are tied to the performance of the company. It would prudent to document your functions and any market research that you have showing how much it would cost to hire someone to perform those same functions (e.g. online salary info, etc.).

Are we allowed to have our current company buy a building and lease it to the new C-corp, as this lowers the debt level of the new corporation and could create more favorable in securing credit needed to fund the business?

This will certainly not work if the existing corporation is owned by you personally. It is a prohibited transaction for a corporation that is funded with your retirement funds (via a 401k Business Financing transaction) to enter into a lease with another entity that you own.

Can an SBA Loan be used in conjunction with the business financing 401k plan?

Our clients regularly use our 401(k) business financing plan in conjunction with an SBA loan – including using the proceeds of the ROBS 401K rollover as a “down-payment” to secure the SBA loan for their business. In fact, the SBA guidelines contemplate that the borrower of an SBA loan could be a corporation that is owned by a 401(k) plan (i.e. a corporation that has been funded via a ROBS transaction). In order to close on your loan, the SBA provider will require you to provide certain documentation. As part of our services, My Solo 401k Financial will help you complete a number of items on this “checklist” so that you can close on your loan and fund your business as quickly as possible.

If my ROBS 401k (business financing 401k) only owns a minute/small amount of my C-Corp business can my business elect S-corp tax status?

Good question. As long as you own part of the C-corporation via your 401k the C-corporation must be taxed as a C-corporation (NOT as an S-Corporation). This is an IRS regulation.

Which state should the corporation business be formed in, Delaware?

Ultimately, we will form the Corporation in whichever state you direct us to do so. Based on customer feedback, most of our customers prefer to set up the Corporation in the state where they will do business and live. Otherwise, they will need to maintain the Corporation in multiple states. Moreover, if you form in a different state you would need to hire a resident agent to serve in the state in which you elect to form the corporation as well as register the corporation in the state in which it operates among possibly other requirements (e.g., filing taxes in multiple states, etc.). For these reasons, the vast majority of our clients elect to form the corporation in the state in which the business operates. Based on customer feedback, setting up the Corporation in Delaware is something to consider if you are looking to attract institutional investors who prefer to invest in Delaware C corporations (e.g. hedge fund, private equity, etc.)

Any recommendations as to what banks are friendliest for the business bank account?

While we don't have any particular banks to recommend, one practical consideration would be to take a long-term view in choosing a bank to open the business bank account at (e.g., one where you could leverage an existing relationship or one where you might build a relationship).

How is the stock investment by the business financing ROBS 401k in the Corporation tracked by the ROBS 401k brokerage firm?

The brokerage firm is merely the custodian of the cash (and other traditional investments such as any mutual funds, publicly traded stocks, etc.) in the ROBS 401k. As such, the brokerage firm will not be holding the stock certificates & therefore the stock certificates are not listed on the brokerage statement which is correct for the reasons mentioned.

What’s the process for executing an in-kind distribution and reporting it. If I made the distribution out my shares, would there be a penalty since I am eligible to take a distribution (age 64)?

If you take an in-kind distribution of the shares from the 401k to yourself, this means that you would have to pay taxes (not penalties if you are older than 59.5) based on the value of the shares and which value needs to be supported by a third party valuation. If you wish to proceed, please obtain a valuation and then let us know so we can guide you through the required steps, and perform the required Form 1099-R reporting

Does doing ROBS Business Financing 401k make you trapped into a set business structure indefinitely?

No it does not. The nature of the business activity can change and/or you can add lines of business. Below is a description of the framework requirements:

- The business must be an active business (e.g. providing goods and/or services)

- You must be active in the operation of the business.

- The business must be operated via the C-corporation that is funded with your retirement funds.

- If you are buying an existing business, the C-corporation must buy the business from an unrelated third party.

- The entity may have different lines of business which it operates through different subsidiary LLC's provided that the C-corporation should be the majority owner of the subsidiary & the other owners (if any) of the subsidiary must be unrelated and must invest cash in the subsidiary in proportion to their ownership percentage.

I was age 56 when I separated from my previous employer and subsequently transferred my former employer 401k plan to the business financing 401k (ROBS), so can I now distribute some of those funds without paying the 10% early distribution penalty?

I understand that you separated from service from your former employer plan when you were age 55 or older such that distributions from your former employer plan were not subject to the 10% early distribution penalty.

When you transfer the funds to a new employer plan (e.g., the ROBS 401k plan), this exception (age 55 exception) does not “travel” with the transferred funds such that if you are under 59.5 and take a withdrawal from your new employer 401k plan the early distribution penalty will apply.

What are basic examples of prohibited transactions and/or use of ROBS 401k funds?

I understand that you separated from service from your former employer plan when you were age 55 or older such that distributions from your former employer plan were not subject to the 10% early distribution penalty.

Typical examples of the prohibited transaction would involve a transaction between the ROBS 401k funded Corporation and a disqualified person. For example, consider a scenario where you own a medical supply business. In this case, the C Corporation, which is funded with your retirement money and operates the home healthcare business, is prohibited from purchasing medical supplies from the business that you own in your own name since that business is considered to be a disqualified person. Another example of a prohibited transaction would be a scenario where you use personal funds to start this business & then reimbursed yourself with the proceeds of the 401(k) business financing plan which were invested in the C Corporation. Please note that we try to identify these potential issues in the course of our initial discussions with potential ROBS clients as well as our online application for our 401(k) business financing plan which asks about potential related party transactions, other businesses that you may own, etc.

Can my corp take on additional investors at the same share price as my 401k, as long as we haven’t opened for business yet?

The C-corporation can certainly take investments from other investors. If those investors purchase common stock, the stock must be issued at fair market value at the time of the purchase. If the investment is made during the pre-revenue startup phase prior to opening for business the C-corporation can make a reasonable business decision to issue the stock at the same price per share as the price per share for the initial investment of 401k funds.

Can the c-corp own 2 LLCs, one with the property and one with the restaurant operating company, or do the property and business need to be owned by the c corp name?

From a 401k perspective, it would be acceptable for the C-corporation to operate the business via a 100% subsidiary LLC and own the real estate through a separate 100% subsidiary LLC. If you will also use an SBA loan, however, this structure is not compatible with the SBA rules such that the C-corporation would need to both operate the business and own the real estate directly.

We run a farm, the farm operates on land that we lease and on land that we own. We live in a farm dwelling on the land we own and there is a mortgage on the TMK we own for the farm dwelling. We do not include the mortgage on our schedule F for the farm. We need to expand, investing in more land leases, and more farming infrastructure, including a state certified dairy processing facility, which will be on the land we own and barns and milking facilities on land we lease, so will the ROBS 401k work for me?

Unfortunately, your situation will not qualify since you live on the land and there is a mortgage on the land on which you are personally obligated. If you did not live on the land and owned it free and clear, then you would be able to use our 401k Business Financing plan to develop the land into a business. Please let me know if you have any questions.

Do I have to participate in the ROBS 401k?

Yes you have to participate as this is the basis for you to rollover your retirement funds into the ROBS 401k and invest in C-corp. company stock.

Can the subsidiary LLC of my ROBS 401k funded business get an SBA Loan?

From a 401k perspective, the borrower may be the C-corporation or a wholly-owned subsidiary of the C-corporation. This means that it would be acceptable for the borrower to be either or both. In our experience, we have seen both a single borrower as well as co-borrower structures. Either is acceptable provided that an EPC/OC structure is not used.

I have a bank asking me if the ROBS 401k is a registered business in the state of MN?

A ROBS 401k It is a federal retirement trust <wbr>that is regulated by the IRS so it is not registered in any state. It is a qualified plan so the income is tax deferred. The 401k has a separate EIN that is specifically for qualified 401k plans (such that the IRS will know that this is a tax deferred vehicle).

Can my compensation be paid as 1099 income?

If take out a HELOC can I invest those funds in the 401k funded corporation?

If the 401k participants takes a home equity loan, she can use the proceeds of the loan to invest in the ROBS 401k funded business. This investment would count as part of the individua's personal stock investment in the Corporation so shares of stock would be issued to the individual. What is more, the company cannot pay back a loan the 401k participant is personally obligated inclluding a home equity loan. However, the individual can use the reasonable W-2 wages received from the 401k funded business (once the company is generating income to justify your reasonable compensation) to pay back this home equity loan.

Does the ROBS 401k allow for 60 day distributions?

First, you must meet a triggering event in order to take a distribution from a 401k including a ROBS 401k. Distribution triggering events include retirement age (usually age 59 1/2) and no longer working for the employer that sponsors the 401k. Regarding taking a distribution from a 401k plan and then paying back within 60 days, the mandatory federal upfront tax of 20% withholding requirement would still apply. For example, if you distribute $10,000 you will receive $8,000 since a 20% federal tax withholding would apply. You woud still be able to deposit $10,000 within 60 days.

Also, distribution reporting will apply. See the following form the IRS page:

Depositing and Reporting Withheld TaxesPayers report income tax withholding from pensions, annuities, 403(b) plans, governmental section 457(b) plans, and IRAs on Form 945, Annual Return of Withheld Federal Income Tax. Do not report these withheld amounts on Form 941, Employers Quarterly Federal Tax Return. You must furnish Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc. to payees and the IRS. Deposit such income tax withholding with any other nonpayroll withholding reported on Form 945 (e.g., backup withholding). Do not combine the Form 945 deposits with deposits for payroll taxes reported on Form 941 or NRA Withholding taxes reported on Form 1042. Circular E and the separate Instructions for Form 945 include information on the deposit rules for Form 945.For information on withholding and reporting on pensions and annuities paid to foreign persons, refer to Pensions, Annuities, and Alimony (Income Code 15) in Publication 515, Withholding of Tax on Nonresident Aliens and Foreign Entities.

What is the typical timeline for rolling more IRA or 401k funds to the ROBS 401k?

It depends on the financial institution currently holding the IRA or former employer funds that you plan to transfer to the ROBS 401k, but we will assist with in preparing the transfer forms.

Are there any additional costs involved in later transfering more IRA/401k to the existing plan we will establish?

The transfer of IRAs or former employer plan funds to the ROBS 401k at a later date will be covered in our annual fee so no additional fees apply on our end.