Last Updated 9/14/2025

Unlike an IRA where you are not required to be self-employed to open an IRA, a solo 401k requires the individual to be self-employed because a solo 401k is a qualified plan not an IRA. To that end, the solo 401k rules are more complex than the IRA rules; however, there are advantages to solo 401k plans, such as increased flexibility in designing plans, increased contribution and deduction limits, the ability to borrow from the plan, and the option to make large voluntary after-tax contributions.

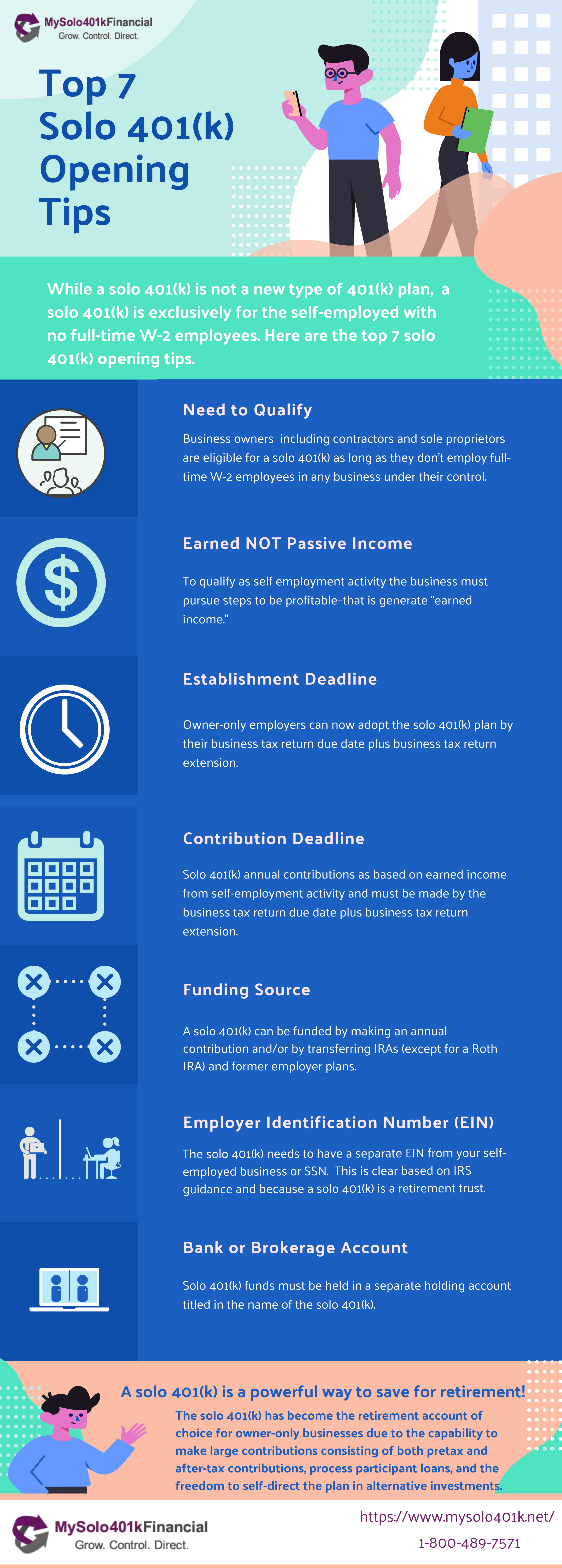

Qualifying:

You must be self-employed to open a solo 401k plan. An individual in business for himself or herself (i.e., contractor, and sole proprietor) is self-employed. Partnerships, LLCs, S-corporation and C-corporations also fall under the self-employed umbrella provided the business owner is performing self-employment activity under the entity.

Earned Income:

In order qualify as self-employment and to open a solo 401k, whether you contribute or no, you need to personally render services to the business. Net earnings include a partner’s distributive share of partnership income or loss (other than separately stated items, such as capital gains and losses). They don’t include income passed through to shareholders of S-corporations. Guaranteed payments to limited partners are net earnings from self-employment if they are paid for services to or for the partnership. Distributions of other income or loss to limited partners aren’t net earnings from self-employment.

Year 2025 Solo 401k Establishment Deadline

The solo 401k setup deadline depends on your self-employed business structure:

Sole Proprietorships & Single-Member LLCs

Good News: Most Flexible Options!

Employee Contributions

- Deadline: Open a Solo 401k and make Employee contributions by April 15, 2026 (No extensions!)

- 2025 Limits:

- Standard: $23,500

- Age 50+: $31,000

- Age 60, 61, 62 or 63: $34,750

Employer & After-Tax Contributions

- Deadline: Open a Solo 401k and make Employer and/or Voluntary After-tax contribution by 4/15/2026 or 10/15/2026 (with timely tax extension)

- Contribution Base: Self-employment income

IMPORTANT NOTE: If you signed up for a Solo 401k by 12/31/2025, all types of 2024 contributions (employee, employer and/or voluntary after-tax) can be made by the self-employed business tax return deadline including extension.

S-Corporations

Employee Contributions

- Deadline: Open the solo 401k by December 31, 2025 and make employee contributions by 3/15/2026 or 9/15/2026 (with timely filed extension)

- 2025 Limits:

- Standard: $23,500

- Age 50+: $31,000

- Age 60, 61, 62 or 63: $34,750

Employer & After-Tax Contributions

- Deadline: Open a Solo 401k by 3/15/2026, or 9/15/2026 if filed a business tax return extension and make Employer and/or Voluntary After-tax contribution by March 15, 2026 or September 15, 2026.

- Contribution Base: W-2 compensation

IMPORTANT NOTE: If you signed up for a Solo 401k by 12/31/2025, all types of 2025 contributions (employee, employer and/or voluntary after-tax) can be made by the self-employed business tax return deadline including extension.

Partnerships & Multi-Member LLCs

Partnership Special Rules Apply

Employee Contributions

- Deadline: Open the solo 401k by December 31, 2025 and make employee contributions by 3/15/2026 or 9/15/2026 (with timely filed extension)

- 2025 Limits:

- Standard: $23,500

- Age 50+: $31,000

- Age 60, 61, 62 or 63: $34,750

Employer & After-Tax Contributions

- Deadline: Open a Solo 401k by 3/15/2026, or 9/15/2026 if filed a business tax return extension and make Employer and/or Voluntary After-tax contribution by March 15, 2026 or September 15, 2026.

- Contribution Base: K-1 self-employment income

IMPORTANT NOTE: If you signed up for a Solo 401k by 12/31/2025, all types of 2025 contributions (employee, employer and/or voluntary after-tax) can be made by the self-employed business tax return deadline including extension.

IMPORTANT

While the SECURE Act extended the deadline to adopt a Solo 401k plan from the end of the year to the business tax return deadline including any timely filed extension, in order to qualify to make employee pretax and Roth contributions in 2026 for the 2025 year the solo 401k plan must be adopted (signed) by December 31, 2025.

If the solo 401k plan is adopted after December 31, 2025 in 2026 but by the business tax return due date plus extension, you will only qualify to make employer profit sharing contributions and voluntary after-tax contributions.

Contribution Deadline

Since a solo 401k plan in a non-ERISA plan, the contribution deadlines are not the same as ERISA plans (e.g., full-time employer 401k and 403b). The contribution deadline for all solo 401k contribution sources (i.e., employee and employer contributions) is the due date of the employer’s tax return as outlined in the above chart.

Funding Sources

As long as you are self-employed, which means you can open a solo 401k plan, you can then elect to fund the plan by making an annual contribution or by transferring/rolling over IRAs (i.e., Traditional, SEP and SIMPLE IRA but not Roth IRAs or after-tax IRAs) and former employer plans.

Employer Identification Number

The solo 401k is a separate entity. For this reason, a separate employer identification number (EIN) is must be obtained in the name of the solo 401k plan. The solo 401k EIN will be also used when opening its funding account (i.e., the bank or brokerage account), for tax reporting and when making alternative investments such as real estate, cryptocurrency, promissory notes, private placements, metals, etc.

Bank or Brokerage Account

You cannot use your personal an/or business bank account to hold the solo 401k funds. As part of our services, we would guide you through the process to set up an account for your Solo 401k. You can have a bank or brokerage account for your solo 401(k), or even both (and we would help you set up the accounts as part of our services). For example, if you wish to have an account at a brokerage like Fidelity or Schwab, we would prepare all of the paperwork that Fidelity or Schwab needs to set up a free account for the Solo 401k (i.e. no set up or maintenance fees) that comes with a free checkbook and through which you can invest in traditional investments (e.g., stocks, mutual funds, bonds, etc.) as well as alternative investments such as real estate, promissory notes, etc. since they are allowed under our IRS-approved plan documents. Please see more at the following links:

Fidelity Brokerage Account with Checkbook & Wire Control

Hire a TPA QUESTION:

Same Solo 401k Plan Name QUESTION:

What happens if I choose a plan name that someone else already has? Example I purchase a real estate property and it is in the name of ABC Trust and four other people are using that name, how would we tell who actually is the real owner of it?

The solo 401k is distinguishable by the employer identification number (EIN) for the plan.

This is similar to individuals with the same name but the individual’s social security number (SSN) is unique.

Transfer IRA to Solo 401k for Syndication Investment QUESTION:

I am actively looking into rolling my traditional IRA over to a Solo 401k with the purpose of investing those funds in syndications. Is this something that will be easily doable with the solok you set up?

Yes pretax IRAs can be transferred to a solo 401k for investing in alternative investments such as a real estate syndication. While we move very fast (e.g. sending you the establishment documents within 1 business) with the solo 401k setup process, the time will come down to how funds are released by the existing provider (and more time if you need to move to a cash position).

Transfer Limit QUESTION:

We have about $56k in my 401k from an old employer that we want to roll into the new solo 401k account. Is a rollover from another 401k account (traditional) going to count as a contribution?

No, transfers to the solo 401k from other retirement plans including former employer 401k plans and IRAs are not subject to a maximum amount and do not count toward the annual solo 401k contribution limit.

Participate in Full-Time Employer 401k & Solo 401k QUESTION:

My employer offers a traditional 401k w/ matching, but the plan does not allow for voluntary after-tax contributions. Can I also open a solo 401k for my self-employed business and make voluntary after-tax 401k contributions?

Yes you can open a solo 401k for your owner-only self-employed business even while also participating in your full-time employer 401k. The voluntary after-tax contributions would be made to the solo 401k and based on the earned income generate from the self-employed business not your day-time employer. Visit here to learn more.

1,000 Hours Exclusion QUESTION:

Could you please provide me where the IRS cites that part-time employees (under 1,000 hours/year) don't disqualify me from opening a solo 401(k)?

- Employees under age 21

- Employees working less than 1,000 hours per year, and as a result do not meet the solo 401k plan's eligibility requirements. See [Treas. Reg. 1.401(k)-1(e)(5)]. Also, a year of service is a computation period during which an employee completes more than 1,000 hours. See [I.R.C. 410(a)(3)(A)].

- Nonresident aliens

- Union employees

Use Robinhood QUESTION:

I have a Solo 401k with you guys. I used Schwab to set up my account. But I'm wondering if I can connect RobinHood and/or Cash App to my Solo401k to buy stocks with too?

In order to do so, the account at Robinhood and/or Cash App would need to be opened in the name an EIN of the solo 401k. In our experience, Robinhood won't open accounts in the name and EIN of a Trust; we are not certain whether Cash App will.

2 Comments

I am a sole proprietor, is it true that I can contribute as an employee up to $19,500 for 2021 and also as an employer? The limits are $58,000 or 25% of my business income, is this correct? I dont need to set up any payroll to pay myself as employee each month, in order to contribute to the solo 401k as an employee, is this correct? Thanks!

Is it possible to use My Solo 401k in a retirement trust account at Vanguard?