As contribution limits continue to rise, the Solo 401(k) remains one of the most powerful retirement plans available to self-employed individuals and small business owners. For tax year 2026, Solo 401(k) contribution limits increased again—creating new opportunities for pretax, Roth, and voluntary after-tax (Mega Backdoor Roth) contributions.

This guide explains how 2026 Solo 401(k) contributions work, who is eligible, how much you can contribute, and how to properly fund and report those contributions.

Video Slides: Years 2025 & 2026 Solo 401k Contribution Limits

General Rules for Making 2026 Solo 401(k) Contributions

Contributions Are Reported on Your Tax Return — Not to the Provider

You do not report your contributions to My Solo 401(k) Financial. Contributions are accounted for by depositing funds into your Solo 401(k) bank or brokerage account, but they are reported on your personal and business tax returns.

Contributions Are Based on Net Self-Employment Income

Solo 401(k) contributions are limited by net income from self-employment. In other words:

You cannot contribute more than you earn.

The definition of “net income” depends on how your business is taxed (sole proprietor, S-corp, partnership, etc.), which is discussed later in this article.

Business or Personal Bank Account Is Allowed

Contributions may be made from either:

-

Your business checking account, or

-

Your personal checking account,

as long as the funds stem from self-employment income.

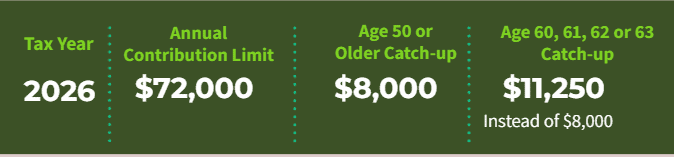

2026 Solo 401(k) Contribution Limits

For tax year 2026, the total Solo 401(k) contribution limit is:

-

$72,000 (under age 50)

-

$80,000 (age 50 or older, includes $8,000 catch-up)

-

$83,250 (ages 60–63, includes $11,250 super catch-up)

These limits apply per participant, even in plans with multiple participants such as spouses.

Mandatory Roth Solo 401k Catch-Up Contributions

Starting in 2026, certain high-paid participants in solo 401(k) plans who wish to make catch-up contributions must make them to the Roth designated accounts within the plan. This requirement will apply to self-employed individuals who had 2025 W-2 (Box 3) wages from their self-employed business that exceeded $150,000. Visit here to learn more.

Super Solo 401k Catch-up Contribution

Those ages 60 to 63 in 2026 have a higher catch-up contribution limit of $11,250 instead of $8,000 thus resulting in being able to contribute $83,250. Click here to learn more.

How to Make a Solo 401(k) Contribution

To fund your Solo 401(k):

-

Make the check payable to the Solo 401(k) plan

-

Write “Annual Contribution” in the memo line

-

Contributions may be made periodically or in a lump sum

You may also use:

-

The MySolo401k online contribution calculator

-

The Annual Contribution Form (for your records only)

Solo 401k Contribution Calculator

You can use our on-line solo 401k contribution calculator to calculate the contribution amount. CLICK HERE.

You may also use the online annual contribution form located on our website to internally document the contribution. This form is for your records only.

https://www.mysolo401k.net/wp-content/uploads/2014/09/Solo_401k_Annual_Contribution_Form.pdf

Understanding the Two Types of Solo 401(k) Contributions

A Solo 401(k) allows the business owner to act as both employee and employer.

Employee Contributions (Elective Deferrals)

For 2026:

-

Up to $24,500

-

Plus $8,000 catch-up (age 50+)

-

Or $11,250 super catch-up (ages 60–63)

If you also contribute to another employer’s 401(k) through a W-2 job, employee contributions are aggregated across all plans.

Employer Contributions (Profit Sharing)

Employer contribution limits depend on entity type:

-

Sole Proprietor / Partnership

→ Up to 20% of net income (after deducting ½ of self-employment tax) -

S-Corporation or C-Corporation

→ Up to 25% of W-2 wages

Total Contribution Cap for 2026

Total contributions (employee + employer + voluntary after-tax) may not exceed:

-

$72,000, or

-

$80,000 (age 50+), or

-

$83,250 (ages 60–63)

Additional information regarding the solo 401k contribution rules.

Solo 401k Contributions

The business owner acts in both capacities in a solo 401k plan: employee and employer. As such, the business owner can make both contribution types: employee and employer. (Note: Matching contributions do not apply to a Solo 401kplan).

Type 1 Contribution (Employee): Employee contributions also known as elective deferrals up to 100% of net earnings from self-employment income up to the annual contribution limit; Note: See information below regarding how to determine your self-employment income for contribution purposes since it depends on how your self-employed business is organized (e.g. sole proprietor, S-Corp, etc.).

2026: $24,500 plus an additional $8,000 catch-up contribution for those 50 or older, or an additional super catch-up contribution of $11,250 for those ages 60-63.

Note: If the Solo 401k participant is participating in another qualified plan such as a 401k plan offered through a w-2 “day job,” any employee contributions made by the individual to such plan will be aggregated with any employee contributions made to the Solo 401k plan in determining whether the limit has been met.

Type 2 Contribution (Employer): Employer profit sharing contributions up to:

- If taxed as an unincorporated business (e.g., sole proprietor or partnership) then 20% of net business income (i.e. from Line 31 on Schedule C or Line 14 of K-1 as applicable) after deducting one-half of self-employment tax; or

- If taxed as a corporation, then 25% of w-2 income.

Multiple Participants

Note: For a solo 401k with multiple participants (e.g. husband and wife), the employee & employer contribution limits are calculated for each participant individually (i.e., based on each person’s self-employment income).

Total Contributions: Total contributions to a solo 401k plan cannot exceed $72,000 for 2026, plus an additional catch-up amount of $8,000 if age 50 or older, or an additional super catch-up contribution of $11,250 for those ages 60-63.

See more regarding making voluntary after-tax contributions below.

IMPORTANT: The annual solo 401k contribution limits depend on the type of entity sponsoring the solo 401k plan.

- If the entity type is a Sole Proprietor, it is equal to line 31 of Schedule C(after deducting one-half of self-employment tax).

- If the entity type is a C-Corporation, it is equal to W-2income from your self-employed business (“Box 1 plus any pre-tax elective deferrals NOT in Box 1).

- If the entity type is an S–Corporation, it is equal to W-2income from your self-employed business (“Box 1 plus any pre-tax elective deferrals NOT in Box 1).

- If the entity type is a Partnership, it is equal K-1 (Form 1065) line 14 from your self-employed business (after deducting one-half of self-employment tax).

Note: To determine the amount equal to one-half of the self-employment tax, please take the following steps:

- Navigate to our online calculator: VISIT HERE.

- For Business Type: select “Unincorporated Sole Proprietorship”

- Enter your net income as applicable (e.g. for a Sole Proprietor enter net income from line 31; for a Partnership enter Line 14 from your K-1).

- Enter your age

- Click “View Report”

- In the sentence beginning “*Calculated as net business income…” the amount equal to one-half of the self-employment tax will appear in the phrase “Self-Employment Tax of ___”

Solo 401k Contribution Deadlines:

The self-directed 401k contribution deadlines are based on the type of entity sponsoring the solo 401k.

- If the entity type is a Sole Proprietorship, the annual solo401k contribution deadline is April 15, or October 15 if tax return extension is timely filed.

- If the entity type is an LLC taxed as an S-Corporation (calendar year), the annual solo 401k contribution deadline is March 15, or September 16 if tax return extension is timely filed.

- If the entity type is an LLC taxed as a Partnership (calendar year), the annual solo401k contribution deadline is March 15, or September 15 if tax return extension is timely filed.

- If the entity type is a Partnership (calendar year), the annual solo 401k contribution deadline is March 15, or September 15 if tax return extension is timely filed.

- If the entity type is an S-Corporation (calendar year), the annual solo 401k contribution deadline is March 15, or September 15 if tax return extension is timely filed.

- If the entity type is an C-Corporation (calendar year), the annual solo 401k contribution deadline is April 15, or October 15 if tax return extension is timely filed.

Plan Year 2026 Annual Solo 401k Contribution Deadlines both Employee and Employer

Making Voluntary After-Tax Contributions

What is the maximum amount of voluntary after-tax contributions that I can make?

You can contribute up to the lesser of (i) 100% of your self-employment compensation (i.e. see below information regarding how to determine your self-employment compensation) or (ii) the overall limit ($72,000 for 2026 contributions) reduced by any pre-tax or Roth employee contributions/salary deferrals and any pre-tax employer/profit sharing contributions.

The amount of self-employment compensation depends on the type of entity sponsoring the solo 401k plan [SEE ABOVE].

When is the deadline to make voluntary after-tax contributions?

The self-directed 401k contribution deadlines are based on the type of entity sponsoring the solo 401k. [SEE ABOVE].

How do I make the voluntary after-tax contributions?

- To make the contribution, you will make the check payable in the name of the solo401k and write “Annual Contribution” on the memo section of the check.

- Deposit the amount of the voluntary after-tax contributions that you elect to make in the separate voluntary after-tax sub-account.

- You will then transfer the funds to the Roth sub-account for the Solo401k. Please let us know right away when you do so that we can send you the applicable forms to capture the information that we need to handle the required 1099-r (which we will do as part of our services for no additional charge).

Where do I report the voluntary after-tax contributions?

- For self-employment income reported on a w-2, you may (but are not required to) report voluntary after-tax contributions in Box 14 of the w-2.

- For all others, there is no place to report voluntary after-tax contributions.

Where do I report the conversion of funds form the voluntary after-tax sub-account to the Roth sub-account?

- A Form 1099-R is used to report the conversion to the IRS.

- On Form 1040, report the amount converted in Line 5a and “0” in Line 4b unless there is a taxable gain. If there is a taxable gain, enter the gain amount. Finally, enter the word “Rollover” next to line 4b.

- A taxable gain would result if the funds in the after-tax account accrued a gain after being contributed to such account in which case the amount of such gain is a taxable and needs to be listed on Line 16b.