If you’re self-employed and looking to supercharge your retirement savings, the Solo 401(k) is one of the most powerful and flexible options available. This blog post breaks down the top essentials you need to know about this plan, including eligibility, contribution rules, investment flexibility, and compliance.

What Is a Solo 401(k)?

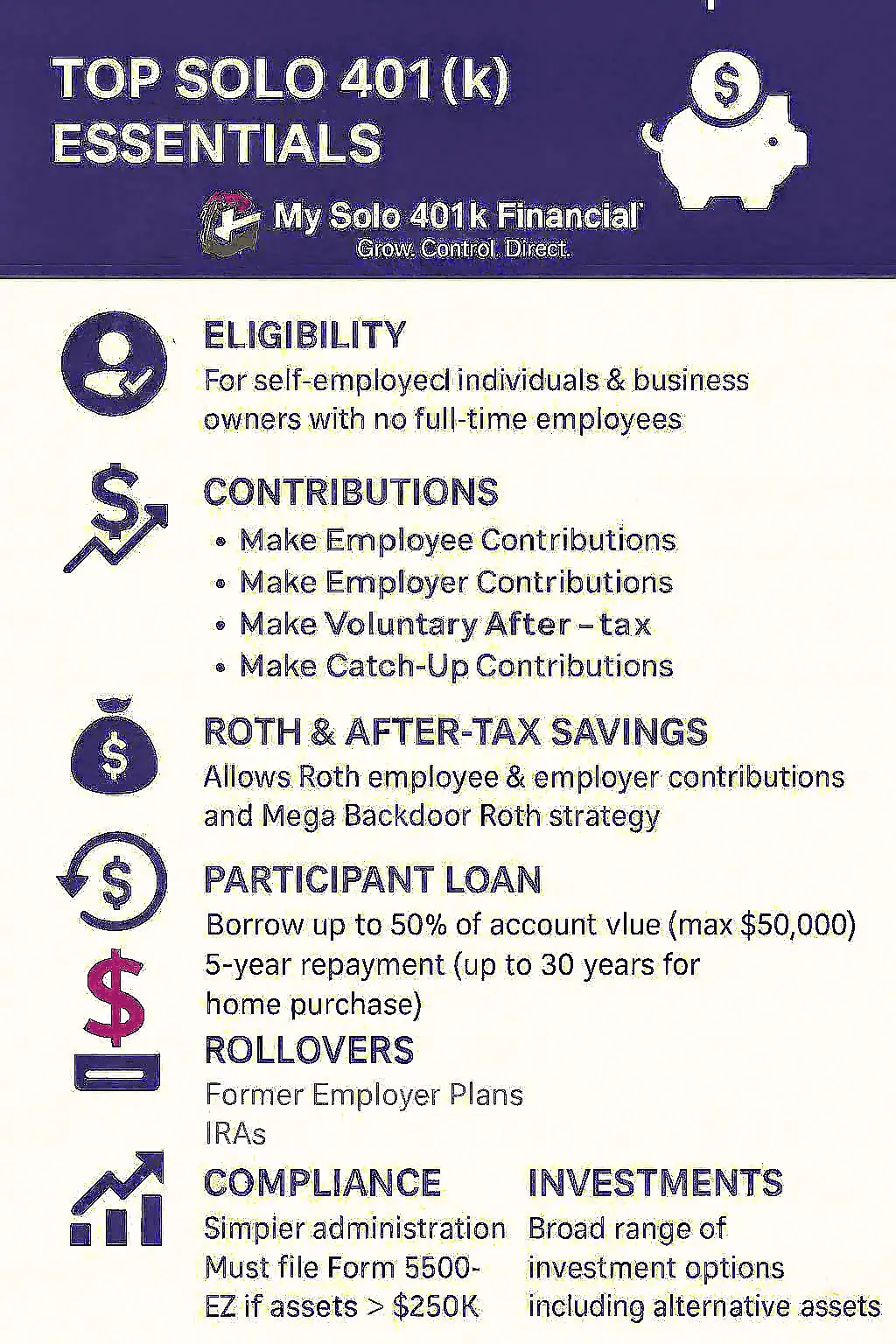

A Solo 401(k) — also known as an individual 401(k), self-directed 401(k), or one-participant plan — is designed specifically for self-employed individuals or business owners with no full-time W-2 employees (other than a spouse).

The plan became widely available following the Economic Growth and Tax Relief Reconciliation Act (EGTRRA) of 2001 and offers more control and flexibility than traditional employer-sponsored 401(k)s.

Who’s Eligible?

Any business entity — sole proprietorship, partnership, LLC, S-corp, or C-corp — can sponsor a Solo 401(k) as long as it has no full-time W-2 employees other than the owner and possibly the spouse. Employees can be excluded if they are:

- Under 21 years old

- Non-resident aliens

- Union members

- Working under 1,000 hours per year

Key Contributions and Limits

Solo 401(k)s allow for both employee and employer contributions, significantly increasing your annual contribution potential.

2024 Limits:

- Employee deferral: Up to $23,000

- Employer contribution: Up to 25% of W-2 wages or 20% of net earnings from self-employment

- Total max: $69,000 (or $76,500 if age 50+)

2025 Limits (projected):

- Employee deferral: Up to $23,500

- Total max: $70,000 (or more with catch-up contributions)

You can also make Roth contributions and voluntary after-tax contributions (used for the Mega Backdoor Roth strategy).

Flexibility With Roth and After-Tax Contributions

Thanks to Secure Act 2.0, both employee and employer contributions can now be Roth. Additionally, voluntary after-tax contributions are allowed and can be converted to a Roth Solo 401(k) or Roth IRA.

Loans and Rollover Capabilities

You can borrow up to 50% of your Solo 401(k) balance, up to a max of $50,000. Rollover options include funds from:

- Former employer 401(k)s

- Traditional IRAs (but not Roth IRAs)

- 403(b), 457(b), and defined benefit plans

Investment Options

Solo 401(k)s support:

- Equities and mutual funds

- Real estate

- Private lending (promissory notes)

- Precious metals (must be stored properly)

- Cryptocurrency

- Alternative assets via checkbook control LLC (optional)

Distributions and Triggering Events

To take distributions, you typically must:

- Be age 59½ or older

- Terminate self-employment

- Or withdraw rollover funds (e.g., from an IRA) at any time

Creditor Protection

Solo 401(k) plans are protected in bankruptcy proceedings and may be protected from general creditors depending on your state’s laws.

Annual Filing: Form 5500-EZ

If your Solo 401(k) exceeds $250,000 in value by year-end, you must file Form 5500-EZ by July 31 of the following year. This is an informational return, not a tax return.

Plan Establishment and Maintenance

To formally establish a plan, IRS-approved plan documents must be executed. Funds must be held at a depository taking financial institution, not personally. Documents in connection to alternative assets (e.g., real estate) may be held by the business owner (i.e., the trustee of the solo 401k plan).

Common Misconceptions

- A Solo 401(k) is not an IRA.

- It is not registered with the state.

- Precious metals must be stored in a depository, not at home.

- Checkbook LLC setups are optional, not required.

Final Thoughts

The Solo 401(k) offers unmatched control and high contribution limits, making it an excellent retirement savings vehicle for solopreneurs. Be mindful of compliance, triggering events, and IRS reporting requirements. Work with a provider that supports your investment strategy and helps you maintain compliance.