If you’re self-employed, run your own business, or even have a side hustle, a Solo 401(k) could be the retirement solution you’ve been overlooking. Whether you’re a freelancer, consultant, real estate or medical professional, or a solo entrepreneur, this powerful retirement account might be your ticket to maximizing savings, minimizing taxes, and staying in control of your investments.

What Is a Solo 401(k)?

A Solo 401(k), also known as an individual 401(k), is a retirement plan designed specifically for business owners with no full-time employees, other than a spouse. It combines the best features of traditional 401(k)s and SEP IRAs, offering higher contribution limits, flexible investment options (including real estate and alternative assets), and loan capabilities.

Who Qualifies?

To qualify for a Solo 401(k), you must:

-

Have self-employment income.

-

Not employ any full-time W-2 employees (1,000+ hours/year), other than your spouse or business co-owners.

Spouses working in the business can also participate and contribute, which can significantly increase household retirement contributions under one plan.

Contribution Limits for 2025

For tax year 2025, each eligible participant can contribute up to $70,000, or $77,500 if age 50 or older. Contribution types include:

-

Employee contributions (up to $23,500 pre-tax or Roth).

-

Employer profit-sharing contributions (up to 25% of W-2 wages).

-

Voluntary after-tax contributions, which can be converted to Roth funds (Mega Backdoor Roth).

Contributions must be supported by W-2 wages if you’re operating as an S-Corporation, or by net self-employment income if you’re a sole proprietor or partnership.

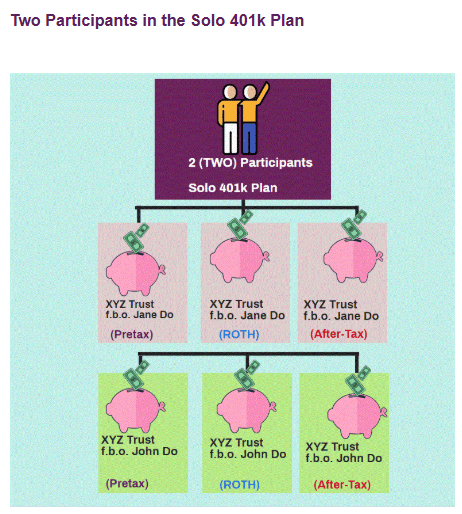

Real-World Example: Jack and Sally

Jack and Sally, owners of an S-Corp, each earn W-2 wages—Jack earns $100,000 and Sally earns $70,000.

-

Jack chooses to contribute:

-

$23,500 as an employee contribution

-

$25,000 as an employer contribution

-

$21,500 as a voluntary after-tax contribution

Total: $70,000

-

-

Sally opts to contribute the entire $70,000 as a voluntary after-tax contribution and later converts it to a Roth Solo 401(k) or Roth IRA.

Both Jack and Sally have separate accounts under the same Solo 401(k) plan.

Roth vs. Pre-Tax vs. After-Tax

-

Pre-Tax Contributions reduce your taxable income now, with taxes paid in retirement.

-

Roth Contributions are made after-tax, grow tax-free, and distributions are tax-free.

-

Employer Roth Contributions are now allowed under the SECURE Act 2.0, but create personal taxable income even though the business gets a deduction.

Comparing to SEP IRAs and Traditional 401(k)s

-

SEP IRAs only allow employer contributions, whereas Solo 401(k)s allow employee, employer, and voluntary after-tax contributions.

-

Traditional 401(k) plans may not allow voluntary after-tax contributions or alternative investments.

-

Solo 401(k)s offer participant loan options (up to $50,000 or 50% of the account balance).

Rollovers and Transfers

You can roll over funds from existing IRAs, former employer 401(k)s, 403(b)s, TSPs, and other qualified plans into a Solo 401(k) without affecting your annual contribution limits. This allows you to consolidate and potentially invest in alternative assets within your Solo 401(k).

Setting Up a Solo 401(k)

Opening a Solo 401(k) with a provider like My Solo 401k Financial is simple:

-

Complete an online application.

-

Receive plan documents to sign and return.

-

Choose your financial institution (bank, brokerage, etc.) to hold the solo 401k funds.

-

Receive assistance with transfers and ongoing support.

Plus, plans set up with My Solo 401k Financial qualify for the Auto Contribution Credit introduced by SECURE Act 2.0—up to $1,500 in tax credits spread over three years (2025–2027), even if you don’t contribute right away.

Fees and Beneficiaries

-

Setup fees must be paid with business or personal funds, not from Solo 401(k) assets.

-

Annual maintenance fees may be paid from the plan, but it’s often better to pay externally to preserve retirement funds.

-

Always name a beneficiary—spouse or living trust—to avoid probate or estate complications.

Final Thoughts

A Solo 401(k) can be a game-changer for those with self-employment income. It offers more flexibility, higher contribution limits, and broader investment choices than most retirement accounts. With options for Roth, pre-tax, and after-tax contributions, plus access to loans and consolidation of old retirement accounts, it’s one of the most powerful tools available to solopreneurs.